Sainsbury Report Final_merged 4p2k54

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report r6l17

Overview 4q3b3c

& View Sainsbury Report Final_merged as PDF for free.

More details 26j3b

- Words: 11,581

- Pages: 38

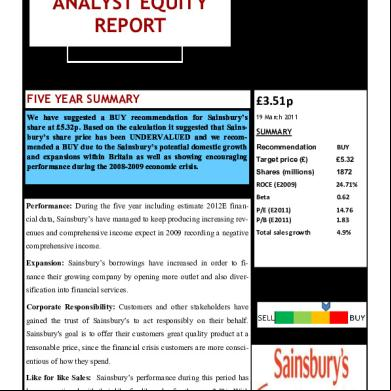

J SAINSBURY’S PLC ANALYST EQUITY REPORT Volume 1, Issue 1

EQUITY REPORT RESEARCH EUROPE

STUDENT ID- 1035280, AFSA

16/01/2013

FIVE YEAR SUMMARY We have suggested a BUY recommendation for Sainsbury’s share at £5.32p. Based on the calculation it suggested that Sainsbury’s share price has been UNDERVALUED and we recommended a BUY due to the Sainsbury’s potential domestic growth and expansions within Britain as well as showing encouraging performance during the 2008-2009 economic crisis.

Performance: During the five year including estimate 2012E financial data, Sainsbury’s have managed to keep producing increasing rev-

£3.51p 19 March 2011

SUMMARY Recommendation

BUY

Target price (£)

£5.32

Shares (millions)

1872

ROCE (E2009)

24.71%

Beta

0.62

P/E (E2011) P/B (E2011)

14.76 1.83

enues and comprehensive income expect in 2009 recording a negative Total sales growth comprehensive income. Expansion: Sainsbury’s borrowings have increased in order to finance their growing company by opening more outlet and also diversification into financial services. Corporate Responsibility: Customers and other stakeholders have gained the trust of Sainsbury’s to act responsibly on their behalf. Sainsbury's goal is to offer their customers great quality product at a reasonable price, since the financial crisis customers are more conscientious of how they spend. Like for like Sales: Sainsbury’s performance during this period has been exceptional with their like-for-like sales for the year 2.3%. With this growth it has enabled the company to maintain a good level of shareholders return (Year 2011 - Annual Report).

4.9%

Company Overview Sainsbury is the third largest British retailer in the UK (Telegraph, 2012). Sainsbury became popular by offering quality dairy products at low prices (Datamonitor 360, 2012) with main strong competitors such as ASDA, Tesco, Marks and Spencer group and Morrison's. Sainsbury also engages in financial service, property investments, fuel as well as retailing such as food other household items. Sainsbury’s have proven to be high successful within the UK with market share of 16.3% (Sainsbury, 2012).

Aim of Report The main focus of this report is to analyse and interpret the financial statement of Sainsbury for a four year period (2008-2011) and also forecast their 2012 statements based on analyst reports and assumptions. This is broken down into different parts for detail breakdown of analysis and interpretation;

The first section will analyse Sainsbury’s financial position while also looking at their credit status which will be compared to Tesco plc and industry average. This will be done with the use of ROCE and credit status ratios.

The second section involves the use of common size and trend analyses to forecast Sainsbury 2012 financial statement based on analyst revenue projection report. I will utilise the CAGR formula to estimate my own judgment of the

Share price movement between Sainsbury's (Blue Line) and Tesco (Red Line) from 2008—2011

Throughout the analysis report for the four years’ timeline (2008-2011), Tesco Plc will be used as Sainsbury comparative competitor. The calculated

revenue figure while also comparing it with the

ratios will be used as a comparison medium between

actual 2012 financial statement..

the two companies. In order to draw conclusions

The final section calculates the company’s fore-

based on their financial performance over the four

casted value of equity per share at the end of the 2011 with the use of Residual Earnings Model.

J SAINSBURY’S PLC

year period.

ID: 1035280

Page 2

Reformulation of Financial Statements For an effective equity analysis, both Sainsbury’s and Tesco’s financial statements (i.e. Balance Sheet, Cash flow Statement and Income Statement) are reformulated. Reformulation of financial statements requires the separation of financing and operating items in the financial statement. This differs from traditional credit analysis which classifies them into current and long term (Penman, 2010). All in all, reformulation provides the following benefits (Penman, 2011); reformulating also help in distinguish different components of income such as core operating income from sales, other core operating income, and unusual items, which facilitates forecasting.

Profitability Analysis Maclaney (2002), states that ratio helps to provide an overview of the business financial condition; it is the first step of assessing Sainsbury’s and Tesco in of performance, liquidity and solvency. The calculated profit analysis ratios (ROCE break-down) will help us establish Sainsbury’s and Tesco historic performance over the period (2008 - 2011) -including the economic downturn in 2007-2008. Ratio analysis for Sainsbury's: Ratios (Level 1&2)

Abbreviations

Return on Common Equity (%) Return on Net Operating assets (%) Operating Profit Margin (%) Asset Turnover Financial Leverage (%) Net Borrowing Cost (%)

ROCE RNOA

Operating Leverage (%)

OLLEV

PM

ATO FLEV NBC RNOA - NBC FLEV x (RNOA-NBC)

2008

2009

2010

2011

13.58 10.70 4.23 2.53 42.88 3.98 6.71 287.87 41.89

-9.05 -4.44 -1.54 2.87 50.46 4.71 -9.14 -461.33 49.54

10.33 7.51 2.72 2.76 45.51 1.32 6.19 281.85 47.27

12.41 9.51 3.44 2.76 40.84 2.41 7.10 289.77 45.88

2008

2009

2010

2011

Ratio analysis for TESCO PLC: Ratios (Level 1 & 2)

Abbreviations

Return on Common Equity (%)

ROCE

21.10

14.40

15.32

16.59

Return on Net Operating assets (%)

RNOA

13.00

7.67

10.58

11.62

Operating Profit Margin (%)

PM

5.33

3.60

4.63

4.94

Asset Turnover

ATO

2.44

2.13

2.28

2.35

Financial Leverage (%)

FLEV

63.00

96.42

69.82

55.71

Net Borrowing Cost (%)

NBC

0.15

0.69

3.79

2.72

RNOA - NBC

12.85

6.98

6.79

8.91

FLEV x (RNOA-NBC)

809.68

673.12

474.16

496.14

OLLEV

50.86

63.59

71.05

73.72

Operating Leverage (%) J SAINSBURY’S PLC

ID: 1035280

Page 3

Profitability Analysis (Continued) ROCE (2008-2011) 25.00 20.00 15.00 10.00 Sainsbury's

% 5.00

Tesco

0.00 -5.00

2008

-10.00

2009

2010

2011

Years

-15.00

Looking at the graph above, it shows that Sainsbury’s ROCE dipped very low in 2009 compared to Tesco. This could be due to credit crunch crises which affected the whole economy especially consumer spending's. There are several value drivers’ ratios that could explain why Sainsbury’s ROCE fell lower than Tesco. However, during the recession Sainsbury till managed to hold 16.1% market share compared to the previous year of 15.8% (Farnham , 2009). Although, Sainsbury’s generated a negative operating profit of (£292.07) during this period. Sainsbury ROCE recovered and rose to 12.41% in 2011, which was gradually increased from a negative (9.05%) in 2009. RNOA ratio for Sainsbury’s showed a negative -4.44% in 2009. This could be due to having a negative operating profit because of the economic crises in 2009 which had an adverse effect on the pension scheme. It resulted in reductions in net operating assets in that year. However, Tesco’s RNOA ratio has been more stable over the four year period compared to Sainsbury’s. In the aftermath of the economic crisis, this made little impact on Tesco’s financial position due to its highly diversified business. Although, Tesco suffered losses on their dirty surplus items such as pension scheme and foreign currency translation, overall it led to a decrease in NOA which relatively led to a low RNOA in 2009. Furthermore, after 2009 both retailers saw growth due to improvements in the economy and thus an increase in consumer confidence. J SAINSBURY’S PLC

ID: 1035280

Page 4

Profitability Analysis (Continued) Operating Profit Margin (PM)- in 2008, 2010 and 2011 both companies had a stable and positive PM. But in 2009, Sainsbury’s had a negative PM which was down to the effect of the economic crisis, this gradually improved by 2010. Regardless of the economic crises both companies still managed to generate increased sales revenue throughout the four year timeline which did not have a major influence on a dramatic increase in cost of sales. Several articles revealed that both retailers implemented price war strategic plans between other competing market share retailers in order to attain a favourable profit margin. Asset Turnover (ATO) Over the four year period,

ATO (2008-2011)

ATO for both firms has been fairly constant consid-

4.00

ering consumer attitudes towards spending in reces-

3.00

sion. Although in 2009 when the economy per-

%2.00 1.00

Sainsbury's

formed poorly, it had a positive effect on Sains-

Tesco

bury’s ATO. Compared to Sainsbury’s in this year,

0.00 2008 2009 2010 2011

Tesco generated a lot more sales revenue than Sainsbury’s during this period. However, Tesco was less

efficient in using its assets to generate revenue in this year in comparison to Sainsbury’s and other years. Sainsbury’s cash flow statement (Cash Investment (I)) shows that the firm invested in t venture and associates - IT services firm (Taylor, 2012) in order to be provide better online services. However, compare to Tesco who invested heavily on PPE which can be concluded to be their highest investment throughout the four years. In order to improve efficiency and ATO overall, Tesco should be cautious in what it invests in during uncertain economic periods. For example, Sainsbury’s did not invest heavily on operating assets but rather utilised existing assets. ATO can also be broken down into different levels such as Inventory and PPE turnover. For the breakdown calculation ATO refer to Appendix 4.1a. On average both Sainsbury’s and Tesco have 2.73 and 2.30 ATO respectively.

Net Borrowing Cost (NBC) - on average both Sainsbury’s and Tesco have 3.11% and 1.83% NBC ratio respectively. Sainsbury’s had the highest NBC between 2008-2009, which worsen in 2010 and gradually improved by 2011. While, Tesco’s NBC was at its lowest in 2008, which gradually improved by 2010. This meant that Tesco cost of borrowings dropped, when interest rate decreased to 2.0% in 2008 (HouseWeb, 2012). This suggested that on average Tesco were better strategically by taking advantage of the fall in interest rate by borrowing more compared to Sainsbury’s who did not make use of the fall in interest rate. The graph below shows the difference in both companies total borrowing (short term and long term) during the four year period. J SAINSBURY’S PLC

ID: 1035280

Page 5

Profitability Analysis (Continued)

Total Borrowings (2008-2011) Axis Title

20000 15000 10000

Sainsbury's

5000

Tesco

0 2008

2009

2010

2011

Years Operating Spread (SPREAD) (RNOA>NBC) - Both Sainsbury’s and Tesco had a desirable Operating Spread over the four year on average (except year 2009), especially in 2011 for Sainsbury’s and 2008 for Tesco. In situations when a positive spread is achieved it means the chances of shareholders receiving greater return are high. This suggests that Tesco and Sainsbury’s have earned more returns on their Net Operating assets to be able to cover the borrowing costs. Sainsbury’s obtained a negative NBC in 2009 as RNOA was less than NBC. Year 2009 was a generally poor economy for both retailers and the general public, it affected Sainsbury’s in which a negative Spread of -9.14% was attained. The manager at Sainsbury did not do a good job i.e. a higher costs of borrowing was incurred due to poor decision making during the financial crises in 2009. The managers went over ‘optimum’ borrowing levels, which meant that all financial liabilities could not be covered by operating income and also it led to attaining a high gearing ratio (FLEV). This could have been avoided if careful attention was paid to financial liabilities and the borrowings of finance was wrongly timed. Operating Liability Leverage - Sainsbury’s have managed to maintain their ratio below 50% while

Tesco’s ratio shows continuous increase throughout the four year period. Tesco’s continuous increase could be due to generated higher operating liabilities and revenues mainly because they have many outlets compared to Sainsbury’s. Sainsbury’s ratio was at its maximum in 2009 and after that it declined.

J SAINSBURY’S PLC

ID: 1035280

Page 6

Profitability Analysis (Continued) Financial Leverage (FLEV) -

Sainsbury’s is not as geared as Tesco’s which ratio stood at 96.4% in

2009, while Sainsbury’s was at 50% for the same year. Tesco’s high gearing ratio was because of the increase in lending in the wake of low interest rate. Overall, it can be said that Sainsbury’s were less risky in comparison to Tesco. One of the main reasons why Tesco was highly geared in 2009 could be due to the fall in interest rate in the UK. Unfortunately, Sainsbury’s did not take advance of the fallen interest rate but rather they played safe in order to avoid huge finance cost due to the uneven market. After 2009, borrowing for both retailers gradually decrease by a low percentage and this was expected to reduced FLEV - this was reflected

in

years

2010

&

2011.

Analysis of Credit Status and other performance ratios For most creditors, they are concerned about a firm’s ability to meet its short-term and long-term obligations through analysing their liquidity, solvency and operating ratios based on the reformulated financial statements i.e. income statement. The commonly recognised ratios will be used to analyse the credit and liquidity status of Sainsbury’s and its competitor Tesco’s. Stock turnover days for both Sainsbury and Tesco have averaged 17 days. Both Sainsbury’s and Tesco have managed to maintain a 14days and 20days stock turnover days respectively which are slightly high but as long as the perishable goods are often rotated. However, both companies also stock domestic items which are less likely to be influenced by technological changes within their holding period. Overall, both retailers have managed to keep an eye on the amount of stock by knowing their Economic Order Quantity (EOQ) which reflected on their steady stock turnover ratios over the four years. Sainsbury’s better performance on this ratio than its competitor is because they hold less stock than Tesco, which means Tesco takes longer to replenish its stocks Debtors Days - Sainsbury’s have a relatively average of four debtor days for the first three years, which

gradually increased to 5days after the financial crises. Due to Sainsbury’s policy, majority of their customer transactions are done on a cash basis which means less credit sales are offered to customers. Compared to Tesco which has increasing debtors days, this could signify that credit sales are offered to customers in order to generate more revenue. Due to high diversification by Tesco in the market, there is incentive to increase their debtors to increase customers. J SAINSBURY’S PLC

ID: 1035280

Page 7

Analysis of Credit Status/ other performance ratios (Continued) Sainsbury’s other ratios Other Performance Ratios Debtors Days Creditors Days Current Ratio(:1) Quick Ratio(:1) Stock Turnover Days Interest Cover (times) Gross Profit Margin(%) Cash Flow to Sales(%) Cash Flow to Assets(%)

2008

2009

2010

2011

4.22 49.43 0.66 0.40 14.76 4.02 5.62 5.08 8.96

3.76 50.80 0.55 0.31 14.07 4.55 5.48 5.38 10.13

3.93 47.67 0.66 0.41 13.57 4.80 5.42 5.47 10.07

5.93 47.53 0.58 0.31 14.86 7.34 5.50 4.51 8.35

Tesco’s other ratios Other Performance Ratios Debtors Days Creditors Days Current Ratio(: 1) Quick Ratio(t:1) Stock Turnover Days Interest Cover (times) Gross Profit Margin(%) Cash Flow to Sales(%) Cash Flow to Assets(%)

2008

2009

2010

2011

10.12 60.82 0.61 0.38 20.31 11.46 7.67 7.83 12.27

12.08 62.08 0.78 0.63 19.44 6.94 7.76 8.43 9.94

12.11 65.89 0.73 0.56 19.04 6.03 8.10 9.40 11.62

13.86 68.49 0.67 0.49 20.66 8.01 8.30 7.36 9.50

Creditors Days - Creditor’s days for Sainsbury’s and Tesco reveals that they both obtain payments from their debtors first before paying their creditors. This should reflect a better working capital for both retailers. In 2009, it took Sainsbury’s few days longer than average to pay their creditors due to the economic situation. However, Tesco’s creditor’s days continued to rise which meant they took longer to pay their creditors than Sainsbury’s after 2009. This could have been the result of a stronger relationship between Tesco and its suppliers resulting in stronger cash flow statement. Sainsbury’s suppliers on the other hand, seems to requests their payment earlier after 2009 - which is reflected on their ratio i.e. decreasing (20092011). Current Ratio - The higher the current ratio, the more capable the company is of paying its obligations (Investopedia 2012). Sainsbury’s and Tesco were able to cover their short-term financial obligations but the ratio was not strong enough. On average, Sainsbury’s has (0.61:1) while Tesco had (0.70:1). However, in 2011 Sainsbury’s ratio dropped slightly which was below the industry average when industry average was at 0.60:1(Thomson One Banker, 2013). Over the four year period, Sainsbury’s current ratio seems rather unpredictable, while Tesco’s current ratio increased from 2008-2010 and later decreased slightly by 2011. The fall in interest rate cause Tesco’s increased current ratio which led to Tesco borrowing more and having more cash in hand in order to survive during the financial crises. While Sainsbury’s utilised their liquidity assets for promotion and marketing which seemed profitable and generated increased sales revenue, but worsened current ratios. J SAINSBURY’S PLC

ID: 1035280

Page 8

Analysis of Credit Status/ other performance ratios (Continued) Quick Ratio- is an indicator of short term liquidity and also the ability for the companies to meet its short

term obligation without the use of its liquid assets. The ratio calculated for Sainsbury’s and Tesco show the ability to both of them surviving without relying on stock (inventory). Sainsbury’s ratio is rather unstable and unpredictable either it will increase or decrease. Unlike Tesco, thia ratio increased from 2008-2010 and later decreased in 2011. The calculated ratio signifies that on average Tesco relies more on their stock compared to Sainsbury’s. The decline in Sainsbury’s quick ratio may have resulted from Sainsbury’s missed opportunities to borrow funds when interest rates were low, as cash held declined slowly over the four year periods. Moreover in 2011, Sainsbury’s held the least cash in comparison to other years and also industry average ratio is the ratio the same as Sainsbury’s ration 0.31:1 (Thomson One Banker, 2013)

Sainsbury's Quick & Current Ratio

Tesco's Quick & Current Ratio

0.50

Ratio(:1)

Ratio(:1)

1.00 Quick Ratio

0.00 2008

2009

2010

2011

Current Ratio

1.00 0.50

Quick Ratio

0.00 2008 2009

2010 2011

Current Ratio

Years

Years Gross Profit - Sainsbury’s gross profit ratio

Gross Profit Margin

appears to be decreasing from 2008-2010. But regardless of the decrease in the ratio,

10.00

creasing healthy revenue each year. However,

%

Sainsbury’s still managed to maintain in5.00

Sainsbury's

cost of sales also increased which contributed to the slight decrease in the ratio. On the other hand however, Tesco’s ratio showed a con-

Tesco

0.00 2008

2009

2010

2011

Years

tinuous increase in its gross profit ratio which

was mainly due to the increase in sales turnover. The fall in Sainsbury’s ratio could be due to lack of bargaining power in of negotiations with their creditors in order to receive better discounts for goods. Sainsbury’s ratio in 2011 seems to be above the industry average which was at 6.85. This means on average they are performing okay. J SAINSBURY’S PLC

ID: 1035280

Page 9

Analysis of Credit Status/ other performance ratios (Continued) Cash flow to Assets – this ratio helps to measures how well a company is able to generate operating cash from its current operating activities. Both Tesco’s and Sainsbury’s ratios has been unstable over the timeline. The ratio is affected when either of the retailers invests or sells fixed assets or an increase/decrease in cash from operations. Sainsbury’s was very efficient in 2009 as Tesco was also in 2008. Nevertheless, in 2011 both retailers’ total assets were at the highest which made the ratio to fall to its lowest. As a result, both retailers were not efficient in maximising the full capacity of their assets as less cash was generated from operations. Cash flow to Sales –the higher the ratio the better, because it indicates the level the company’s financial strength. The ratio also indicates the ability for both Sainsbury’s and Tesco to translate their sales into cash (proportion of cash from operations in overall sales). Both companies experienced an improvement in the ratio up until 2010. The decrease in 2011 was due to both companies experiencing a decrease in cash from operations as sales continued to rise. I personally think that the increased rate at which Tesco offered credit sales to their customers might have had an adverse impact on the ratio.

Interest Cover - A high interest cover ratio means that a business can easily meet its interest obligations from profits (Bized, 2012). The ratio tells how easily Sainsbury’s and Tesco’s can pay interest on their outstanding debts. Sainsbury’s had much lower interest cover in comparison to Tesco’s over the four year timeline. Which means Tesco can cover their interest debt many times than Sainsbury’s. For example, Tesco were able to cover their interest twelve times in 2008 while Sainsbury could only cover theirs four times. Again, based on the financial crisis in 2009 Tesco’s ratio decreased, this could also be due to increase in borrowings while Sainsbury’s ratio still gradually increased from 2008 - 2011. A lower interest cover could mean danger to a business, but luckily

Interest Cover

Sainsbury ratio peaked in 2011 mainly because Sains14.00

bury’s finance cost was at its lowest during this period.

12.00

Overall, Sainsbury’s ratio was much lower than total borrowings (short and long term borrowings) in

Times

Tesco’s, this could be due to Sainsbury’s have a lower

10.00 8.00

Sainsbury

6.00

Tesco

4.00

comparison to Tesco’s . It is still uncertain why Sains-

2.00

bury’s borrowed lesser amount when they could have

0.00 2008

2009

2010

2011

taken the advantage of a reduce interest rate at 0.5%.

J SAINSBURY’S PLC

ID: 1035280

Page 10

Forecasting and Share Price Valuation This part aims to explain how Sainsbury’s forecasted equity share price was arrived at the end of the fourth year (2011). Based on my evaluation, the calculated value of Sainsbury’s share might help investors into making the right decision on either to buy, sell or hold Sainsbury’s shares. By using Residual Earnings Model which is the most commonly used model by analyst (Investopedia, 2012) , the share price calculated by using this model will be compared to the actual share price of Sainsbury’s as at 19th March 2011.

In order to calculate my own estimation of 2012’s revenue, I made use of the “Compound Annual Growth Rate (CAGR)” - RBS (analysts) use the same method for forecasting (Scarborough, 2012). I chose to use this model for forecasting 2012 revenue and used the common size and trend analysis to forecast

the

rest

of

the

income

statement.

The formula s for growth rate changes from year to year (4.29%) which was later multiplied with 2011 revenue in order to arrive at my own predictions of 2012 revenue figure - which was close to the actual and other analyst revenue figures. The analyst revenue figures includes macro-economic factors such as cost of inflation, but these predictions varies from analyst to analyst so it can tend to be subjective.

CAGR Model Rate

4.29%

Year 2011 Revenue

£21102

CAGR Model Revenue

£22007

Analyst Revenues

£

RBS

22540

Evolution Securities Plc

22085

Santander

22325.6

My predicted Revenue was quite close to the actual 2012 Revenue (£22,294 m). The next stage was to gather twenty four years’ worth of Sainsbury’s share prices and FTSE ALL SHARE price index (Appendix 1.3a). I was able to calculate the return index for both Sainsbury’s and FTSE ALL SHARE. This enabled to arrive at a beta by using the regression analysis tool.

J SAINSBURY’S PLC

ID: 1035280

Page 11

Forecasting and Share Price Valuation Continuation ANOVA df Regression Residual Total

Intercept X Variable 1

SignifiSS MS F cance F 1 0.260358339 0.260358 52.47244 4.03E-12 287 1.424039673 0.004962 288 1.684398012

Coeffi- Standard ErLower Upper cients ror t Stat P-value 95% 95% 0.001231 0.004166711 0.295457 0.767858 -0.00697 0.009432 0.618599 0.085397227 7.243787 4.03E-12 0.450515 0.786684

Lower 95.0% -0.00697 0.450515

Upper 95.0% 0.009432 0.786684

By using a regression analysis tool I was able to arrive at Sainsbury’s Beta which was later used in conjunction with CAPM to calculate Sainsbury’s ‘Cost of Equity’. CAPM can be described as “a model that describes the relationship between risk and expected return and that is used in pricing risky securities” (Investopedia, 2013)

(Investopedia, 2013)

Through this method (CAPM) I was able to arrive at Sainsbury’s cost of equity at 7.58%. The true worth of a company’s share price is very important to shareholder and other stakeholders (such as investors) in order to aid them in buying or selling shares. The calculated forecasted value of equity per share was estimated based on Evolution Security Plc (analyst) forecasted revenue estimate and the actual 2011 data. The ‘Residual Earning Model’ has been used to value Sainsbury’s share price as at the end of March 2011. Three different assumptions have been put into perspective when using this formula to calculate the earnings per share. While calculating the third case perspective (Case 3), 0.7% economic GDP was used since retailer industry has been growing in line with the economy which was at 0.7% in 2011 (BBC, 2012).

J SAINSBURY’S PLC

ID: 1035280

Page 12

Forecasting and Share Price Valuation Continuation Valuation : Residual Earnings (RE) Model 2011 (£m)

E2012 (£m)

Reformulated Income statement Operating income

726.48

773.11

-53.48

-51.87

673.00

721.24

Net financial expenses Comprehensive income (included the amount for MI)

Reform. Balance Sheet Net operating assets

7639.00

Net financial obligations Ordinary shareholders' equity (included MI)

2215 5424.00

310.1

Residual Earnings

Case 1: Assume that RE after 2012 would be zero because of strong competition in the industry. 5712.25 Intrinsic value of BT's equity in 2011 3.05 Intrinsic per share value (£’s) 1.05 Intrinsic P/B 8.49 Intrinsic P/E Case 2: if it assumes that REs after 2012 will remain as 310.1 forever. Intrinsic value of BT's equity in 2011 Intrinsic per share value (£’s) Intrinsic P/B Intrinsic P/E

Case 3:Assuming the growth rate is 0.7% based on the economy GDP Intrinsic value of BT's equity in 2011 Intrinsic per share value (£’s) Intrinsic P/B Intrinsic P/E

9515.04 5.08

1.75 14.14

9931.28

9931.28

5.31

1.83 14.76

Additional information: Share price of Sainsbury on 19 March 2011 is £3.51, source: Sainsbury's Annual Report Therefore, the market over values Sainsbury's share From my calculation Cost of Equity is 7.58% No. of shares outstanding is 1872 million, from Sainsbury 2010/2011 annual report.

J SAINSBURY’S PLC

ID: 1035280

Page 13

Analyst Share Price Assumption Evolution Securities– this analyst initiated a Reduce because Sainsbury’s did not deliver the total sales growth target of 8% but rather they achieved 7.5%. And also the analyst believe that with Sainsbury’s underling growth which were currently unimpressive, in addition with market deterioration and growth rate getting weaker due to inflation. Evolution urges investors to sell Sainsbury’s shares at a target price of 350p. Santander– However, this analyst suggested a Hold of Sainsbury’s share at target price of 400p due to Sainsbury’s attaining three times growth on non-food items which driven by Sainsbury’s opening new outlets in order to boost sales. This means that management strategies have proven to be successful and can be seen in the foreseeable future. RBS– finally, RBS suggested a Hold at the target price of 370p. This is due to Sainsbury’s performing very well in the third quarter or 2011. Although sales growth target are not been achieve, RBS are positive Sainsbury’s can have continuous development in their business model.

SUMMARY The Residual Earnings Model suggests that Sainsbury’s share price should be currently at a value of £5.31. In comparison to the actual share price of £3.51 as at 19th March 2011. The estimated share price is different from the actual which means that the market has undervalued Sainsbury’s shares. Residual earnings model assumes three different cases in calculating the share price of Sainsbury’s. RBS suggested that investors should Hold on the bases that the share price is likely to increase between the financial year of 2010-2013 and with EPS CAGR of 10%. In conclusion, the market has undervalued Sainsbury’s share and I believe that it has the potential to rise to the target price of £5.31. I would advice investors to buy and hold.

J SAINSBURY’S PLC

ID: 1035280

Page 14

APPENDICES 1.1 – SWOT ANALYIS OF J SAINSBURY’S Strengths

Weaknesses

Significant market presence in the UK

Robust portfolio of own-labelled products

Concentration of operations in the UK could affect the performance in case of any unfavourable economic scenario

Strong results in tough economic and macro environment

High debt burden

Opportunities

Threats

Growth opportunities in the Chinese and Indian economies

Rising labour cost in the UK

Weak consumer spending in the UK

Growth potential in the online distribution channel

Intense competition

Rise in demand for organic foods

Datamonitor 360 (2012)

APPENDICES 1.2– INDUSTRY AVERAGE AS AT 19TH MARCH 2011 Industry Benchmark Ratio analysis : Credit Status Ratios

2011

Stock Turnover Days

23.00

Current Ratio (to 1)

0.60

Quick Ratio (to 1)

0.31

Debtors Days

11.48

Gross Profit Margin(%)

6.85

Cash Flow to Sales(%)

5.66 Thomson One Banker, (2013)

J SAINSBURY’S PLC

ID: 1035280

Page 15

APPENDIX 1.3a DATASTREAM DATA OF SAINSBURY AND FTSE ALL SHARE RETURNS Start

19/02/1987

End Frequency

Name

19/03/2011 M

SAINSBURY (J) PRICE - LNGBP

FTSE ALL SHARE PRICE INDEX

Code

926002(P.LNGBP)

FTALLSH

CURRENCY

£

£

19/02/1987

235.31

960.83

19/03/1987

244.14

994.65

19/04/1987

234.33

979.12

19/05/1987

260.81

1103.1

19/06/1987

284.34

1137.25

19/07/1987

279.43

1234.49

19/08/1987

257.86

1120.81

19/09/1987

274.26

1188.42

19/10/1987

232.37

1074.58

19/11/1987

224.53

824.11

19/12/1987

218.65

867.07

19/01/1988

223.55

902.5

19/02/1988

212.76

889.24

19/03/1988

232.37

951.46

19/04/1988

241.2

925.79

19/05/1988

218.65

909.69

19/06/1988

220.61

956.27

19/07/1988

218.65

961.03

19/08/1988

213.74

961.62

19/09/1988

197.57

912.59

19/10/1988

202.96

968.26

19/11/1988

199.04

951.59

19/12/1988

189.23

913.05

19/01/1989

207.86

985.45

19/02/1989

228.94

1058.89

19/03/1989

217.66

1076.71

19/04/1989

225.51

1076.35

19/05/1989

237.27

1131.41

19/06/1989

260.81

1103.16

19/07/1989

259.82

1170.28

19/08/1989

281.4

1204.75

19/09/1989

279.43

1198.2

19/10/1989

247.08

1100.15

19/11/1989

250.02

1115.15

19/12/1989

253.94

1168.64

19/01/1990

256.88

1169.46

19/02/1990

257.86

1147.05

Return

0.037525 -0.04018 0.113003 0.090219 -0.01727 -0.07719 0.0636 -0.15274 -0.03374 -0.02619 0.02241 -0.04827 0.09217 0.038 -0.09349 0.008964 -0.00888 -0.02246 -0.07565 0.027281 -0.01931 -0.04929 0.098452 0.101414 -0.04927 0.036065 0.052148 0.099212 -0.0038 0.083058 -0.007 -0.11577 0.011899 0.015679 0.011578 0.003815

Return (FTALLSH)

0.035198734 -0.015613532 0.126623907 0.030958209 0.085504506 -0.092086611 0.060322445 -0.09579105 -0.233086415 0.052128963 0.040861753 -0.014692521 0.069969862 -0.026979589 -0.017390553 0.051204256 0.004977674 0.000613925 -0.050986876 0.061002203 -0.01721645 -0.040500636 0.079294672 0.074524329 0.016828944 -0.000334352 0.051154364 -0.024968844 0.060843395 0.02945449 -0.005436813 -0.08183108 0.013634504 0.047966641 0.00070167 -0.01916269

19/03/1990

256.88

1111.57

19/04/1990

247.08

1085.2

19/05/1990

266.69

1117.16

19/06/1990

273.55

1168.35

19/07/1990

296.1

1171.71

19/08/1990

285.32

1065.7

19/09/1990

298.06

1000.73

19/10/1990

301.99

1010.12

19/11/1990

290.22

1009.06

19/12/1990

302.97

1046.13

19/01/1991

307.87

1006.8

19/02/1991

322.58

1115.14

19/03/1991

340.22

1197.98

19/04/1991

362.77

1220.16

19/05/1991

370.62

1188.02

19/06/1991

339.24

1194.88

19/07/1991

368.88

1213.66

19/08/1991

349.05

1216.23

19/09/1991

351.03

1253.48

19/10/1991

354.01

1252.83

19/11/1991

327.23

1190.42

19/12/1991

346.07

1146.78

19/01/1992

362.93

1213.08

19/02/1992

365.91

1216.45

19/03/1992

375.82

1186.78

19/04/1992

420.44

1268.47

19/05/1992

463.58

1312.07

19/06/1992

464.07

1248.12

19/07/1992

445.23

1168.05

19/08/1992

434.33

1122.95

19/09/1992

426.89

1204.37

19/10/1992

472.01

1206.68

19/11/1992

486.88

1284.33

19/12/1992

547.87

1333.41

19/01/1993

554.31

1330.19

19/02/1993

516.13

1387.47

19/03/1993

520.6

1421.34

19/04/1993

462.09

1387.43

19/05/1993

455.15

1393.51

19/06/1993

479.94

1422.43

19/07/1993

454.16

1408.73

19/08/1993

511.67

1521.01

19/09/1993

446.23

1494.29

19/10/1993

405.57

1545.92

19/11/1993

387.72

1533.12

19/12/1993

446.23

1640.19

19/01/1994

473

1743.78

19/02/1994

362.93

1703.02

19/03/1994

384.75

1624.88

-0.0038 -0.03815 0.079367 0.025723 0.082435 -0.03641 0.044652 0.013185 -0.03897 0.043932 0.016173 0.04778 0.054684 0.066281 0.021639 -0.08467 0.087372 -0.05376 0.005673 0.008489 -0.07565 0.057574 0.048718 0.008211 0.027083 0.118727 0.102607 0.001057 -0.0406 -0.02448 -0.01713 0.105695 0.031504 0.125267 0.011755 -0.06888 0.008661 -0.11239 -0.01502 0.054466 -0.05372 0.126629 -0.12789 -0.09112 -0.04401 0.150908 0.059991 -0.23271 0.060122

-0.03093152 -0.023723202 0.029450792 0.045821547 0.002875851 -0.090474605 -0.060964624 0.00938315 -0.00104938 0.036737161 -0.03759571 0.107608264 0.074286637 0.018514499 -0.026340808 0.005774314 0.015717059 0.002117562 0.030627431 -0.000518556 -0.049815218 -0.03665933 0.057814053 0.002778053 -0.024390645 0.068833314 0.034372118 -0.048739778 -0.064152485 -0.038611361 0.072505454 0.001918015 0.064350118 0.038214478 -0.002414861 0.043061518 0.024411339 -0.023857768 0.004382203 0.020753349 -0.009631405 0.079702995 -0.017567274 0.034551526 -0.008279859 0.069837977 0.063157317 -0.023374508 -0.045883196

19/04/1994

355.99

1582.94

19/05/1994

390.7

1571.99

19/06/1994

413.01

1515.01

19/07/1994

396.65

1540.95

19/08/1994

436.31

1598.16

19/09/1994

432.34

1543.64

19/10/1994

395.65

1524.39

19/11/1994

417.47

1554.22

19/12/1994

395.16

1505.86

19/01/1995

416.48

1503

19/02/1995

413.5

1505.8

19/03/1995

423.91

1513.96

19/04/1995

413.5

1556.15

19/05/1995

435.81

1605.78

19/06/1995

441.27

1654.2

19/07/1995

459.12

1674.67

19/08/1995

465.56

1728.26

19/09/1995

455.15

1745.57

19/10/1995

419.45

1757.31

19/11/1995

378.8

1769.5

19/12/1995

363.92

1754.28

19/01/1996

413.5

1831.99

19/02/1996

382.76

1843.95

19/03/1996

372.85

1835.38

19/04/1996

358.47

1924.17

19/05/1996

382.76

1901.77

19/06/1996

388.71

1883.36

19/07/1996

370.86

1841.45

19/08/1996

402.59

1908.96

19/09/1996

371.85

1957.02

19/10/1996

353.01

1987.45

19/11/1996

362.43

1954.08

19/12/1996

375.82

1979.85

19/01/1997

393.17

2061.07

19/02/1997

313.35

2121.75

19/03/1997

325.74

2115.4

19/04/1997

324.26

2092.44

19/05/1997

363.92

2211.91

19/06/1997

358.96

2210.2

19/07/1997

424.91

2284.14

19/08/1997

437.3

2317.83

19/09/1997

443.75

2362.31

19/10/1997

461.6

2480.18

19/11/1997

472.5

2285.91

19/12/1997

484.9

2361.28

19/01/1998

499.28

2467.54

19/02/1998

449.7

2647.24

19/03/1998

502.75

2797.33

19/04/1998

477.96

2777.16

-0.07475 0.097503 0.057103 -0.03961 0.099987 -0.0091 -0.08486 0.05515 -0.05344 0.053953 -0.00716 0.025175 -0.02456 0.053954 0.012528 0.040451 0.014027 -0.02236 -0.07844 -0.09691 -0.03928 0.136239 -0.07434 -0.02589 -0.03857 0.06776 0.015545 -0.04592 0.085558 -0.07636 -0.05067 0.026685 0.036945 0.046166 -0.20302 0.03954 -0.00454 0.122309 -0.01363 0.183725 0.029159 0.01475 0.040225 0.023614 0.026243 0.029656 -0.0993 0.117968 -0.04931

-0.025811137 -0.006917508 -0.03624705 0.017121999 0.037126448 -0.034114231 -0.012470524 0.019568483 -0.031115286 -0.001899247 0.001862941 0.005419046 0.027867315 0.031892812 0.03015357 0.012374562 0.032000334 0.010015854 0.006725597 0.006936739 -0.0086013 0.044297376 0.00652842 -0.004647631 0.048376903 -0.011641383 -0.009680456 -0.022252782 0.036661327 0.025176012 0.015549151 -0.01679036 0.013187792 0.04102331 0.029441019 -0.002992813 -0.010853739 0.057096022 -0.000773088 0.033453986 0.014749534 0.019190363 0.049896076 -0.078328992 0.032971552 0.045001016 0.072825567 0.056696786 -0.007210447

19/05/1998

511.18

2794.62

19/06/1998

515.64

2726.87

19/07/1998

525.06

2882.73

19/08/1998

529.52

2646.95

19/09/1998

540.43

2354.83

19/10/1998

569.19

2348.1

19/11/1998

510.68

2567.36

19/12/1998

460.6

2607.39

19/01/1999

431.85

2730.74

19/02/1999

363.18

2764.7

19/03/1999

359.46

2847.18

19/04/1999

411.52

3010.25

19/05/1999

407.06

2911.37

19/06/1999

381.77

3028.03

19/07/1999

386.98

3030.3

19/08/1999

406.81

2886.03

19/09/1999

409.29

2846.58

19/10/1999

373.34

2799.26

19/11/1999

315.58

3033.78

19/12/1999

326.24

3150.24

19/01/2000

349.05

3069.72

19/02/2000

288.31

2948.99

19/03/2000

251.37

3126.18

19/04/2000

304.67

2937.83

19/05/2000

337.89

2892.43

19/06/2000

298.72

3095.44

19/07/2000

306.41

3102.86

19/08/2000

322.27

3143.84

19/09/2000

361.44

3084.07

19/10/2000

366.9

2977.26

19/11/2000

424.41

3085.5

19/12/2000

409.54

3009.03

19/01/2001

338.14

2992.06

19/02/2001

381.77

2944.93

19/03/2001

369.87

2688.78

19/04/2001

390.7

2818.19

19/05/2001

421.44

2860.21

19/06/2001

422.43

2753.8

19/07/2001

425.4

2628.57

19/08/2001

385.49

2590.61

19/09/2001

366.9

2272.17

19/10/2001

349.79

2406.13

19/11/2001

373.84

2578.75

19/12/2001

347.31

2478.95

19/01/2002

372.85

2487.99

19/02/2002

404.58

2461.12

19/03/2002

392.18

2571.43

19/04/2002

394.66

2548.05

19/05/2002

386.23

2537.41

0.069504 0.008725 0.018269 0.008494 0.020604 0.053217 -0.1028 -0.09807 -0.06242 -0.15901 -0.01024 0.144828 -0.01084 -0.06213 0.013647 0.051243 0.006096 -0.08784 -0.15471 0.033779 0.069918 -0.17402 -0.12813 0.212038 0.109036 -0.11593 0.025743 0.051761 0.121544 0.015106 0.156746 -0.03504 -0.17434 0.129029 -0.03117 0.056317 0.078679 0.002349 0.007031 -0.09382 -0.04822 -0.04663 0.068756 -0.07097 0.073537 0.085101 -0.03065 0.006324 -0.02136

0.006286998 -0.02424301 0.057157107 -0.081790525 -0.110360982 -0.002857956 0.093377624 0.015591892 0.047307844 0.012436189 0.029833255 0.057274215 -0.03284777 0.040070482 0.000749662 -0.047609148 -0.013669297 -0.016623457 0.083779285 0.038387754 -0.025559957 -0.03932932 0.060084978 -0.06024925 -0.015453583 0.07018666 0.002397074 0.01320717 -0.019011782 -0.034632807 0.036355575 -0.024783666 -0.005639691 -0.015751689 -0.086979996 0.048129635 0.014910279 -0.037203562 -0.045475343 -0.014441312 -0.122920856 0.058956856 0.07174176 -0.038700921 0.003646705 -0.010799883 0.044821057 -0.009092217 -0.004175742

19/06/2002

347.06

2270.73

19/07/2002

317.32

1995.47

19/08/2002

325.25

2128.84

19/09/2002

308.89

1852.07

19/10/2002

268.98

1973.16

19/11/2002

290.54

1966.6

19/12/2002

267.74

1850.02

19/01/2003

244.93

1844.77

19/02/2003

225.84

1762.53

19/03/2003

235.01

1803.22

19/04/2003

232.53

1867.76

19/05/2003

257.32

1915.87

19/06/2003

256.83

2018.05

19/07/2003

260.79

2002.16

19/08/2003

288.31

2099.84

19/09/2003

290.79

2111.57

19/10/2003

271.7

2155.15

19/11/2003

295.75

2138.58

19/12/2003

300.21

2175.41

19/01/2004

289.55

2244.62

19/02/2004

296

2253.94

19/03/2004

294.76

2209.84

19/04/2004

277.65

2264.9

19/05/2004

272.45

2217.22

19/06/2004

277.4

2238.01

19/07/2004

257.5

2157.19

19/08/2004

257.5

2166.93

19/09/2004

278

2281.88

19/10/2004

249

2308.58

19/11/2004

270.5

2370.35

19/12/2004

266

2352.37

19/01/2005

272.5

2422.06

19/02/2005

300.5

2534.73

19/03/2005

293.5

2476.21

19/04/2005

291.25

2434.24

19/05/2005

290.75

2472.76

19/06/2005

284.25

2544.59

19/07/2005

280

2600.39

19/08/2005

283.25

2661.32

19/09/2005

283.5

2724.41

19/10/2005

277.5

2587.2

19/11/2005

288.5

2765.34

19/12/2005

309

2803.53

19/01/2006

305.25

2888.41

19/02/2006

318.75

2979.74

19/03/2006

330

3062.18

19/04/2006

341

3102.69

19/05/2006

331

2884.1

19/06/2006

324.75

2865.1

-0.10142 -0.08569 0.024991 -0.0503 -0.1292 0.080155 -0.07847 -0.08519 -0.07794 0.040604 -0.01055 0.10661 -0.0019 0.015419 0.105526 0.008602 -0.06565 0.088517 0.01508 -0.03551 0.022276 -0.00419 -0.05805 -0.01873 0.018168 -0.07174 0 0.079612 -0.10432 0.086345 -0.01664 0.024436 0.102752 -0.02329 -0.00767 -0.00172 -0.02236 -0.01495 0.011607 0.000883 -0.02116 0.03964 0.071057 -0.01214 0.044226 0.035294 0.033333 -0.02933 -0.01888

-0.105099294 -0.121220929 0.066836384 -0.130009771 0.065380898 -0.003324616 -0.059279976 -0.002837807 -0.044580083 0.023086132 0.035791528 0.025758127 0.053333473 -0.007873938 0.04878731 0.00558614 0.020638672 -0.00768856 0.017221708 0.031814692 0.00415215 -0.019565738 0.024915831 -0.021051702 0.009376607 -0.036112439 0.004515133 0.053047399 0.011700878 0.026756708 -0.007585378 0.029625442 0.046518253 -0.023087272 -0.016949289 0.015824241 0.029048513 0.021928877 0.023431101 0.023706281 -0.050363198 0.06885436 0.013810237 0.030276116 0.031619472 0.027666843 0.013229137 -0.070451769 -0.006587844

19/07/2006

334

2932.45

19/08/2006

359.5

3001.06

19/09/2006

372.75

2982.91

19/10/2006

395.25

3149.97

19/11/2006

410.5

3184.87

19/12/2006

408.25

3206.5

19/01/2007

434.25

3229.02

19/02/2007

512.75

3340.86

19/03/2007

557

3220.5

19/04/2007

530

3345.25

19/05/2007

556

3449.69

19/06/2007

581

3436.71

19/07/2007

592

3433.75

19/08/2007

520.5

3128.97

19/09/2007

554

3319.35

19/10/2007

582

3355.25

19/11/2007

408

3135.95

19/12/2007

425.5

3192.35

19/01/2008

399.5

3003.52

19/02/2008

381.5

3053.21

19/03/2008

325

2840.75

19/04/2008

379.5

3090.06

19/05/2008

366.25

3243.48

19/06/2008

322.5

2905.97

19/07/2008

298.5

2735.72

19/08/2008

326.75

2710.74

19/09/2008

370.25

2708.98

19/10/2008

250.5

2050.84

19/11/2008

289.25

1998.02

19/12/2008

321

2141.1

19/01/2009

332.5

2061.15

19/02/2009

336.75

2019.72

19/03/2009

308.5

1931.04

19/04/2009

311.5

2096.6

19/05/2009

346

2285.23

19/06/2009

317.25

2211.91

19/07/2009

316

2239.52

19/08/2009

313.2

2405.57

19/09/2009

335.1

2658.01

19/10/2009

330.1

2715.26

19/11/2009

331.9

2695.15

19/12/2009

316

2653.36

19/01/2010

339.5

2815.68

19/02/2010

333.4

2741.54

19/03/2010

333.1

2891.94

19/04/2010

344.8

2940.74

19/05/2010

323

2662.27

19/06/2010

331.7

2711.62

19/07/2010

346.4

2658.05

0.028483 0.076347 0.036857 0.060362 0.038583 -0.00548 0.063686 0.180771 0.086299 -0.04847 0.049057 0.044964 0.018933 -0.12078 0.064361 0.050542 -0.29897 0.042892 -0.0611 -0.04506 -0.1481 0.167692 -0.03491 -0.11945 -0.07442 0.09464 0.133129 -0.32343 0.154691 0.109767 0.035826 0.012782 -0.08389 0.009724 0.110754 -0.08309 -0.00394 -0.00886 0.069923 -0.01492 0.005453 -0.04791 0.074367 -0.01797 -0.0009 0.035125 -0.06323 0.026935 0.044317

0.023507033 0.023396818 -0.006047863 0.056005713 0.011079471 0.006791486 0.007023234 0.034635896 -0.036026652 0.038736221 0.031220387 -0.003762657 -0.000861289 -0.088760102 0.060844303 0.01081537 -0.065360256 0.017984981 -0.059150782 0.016543922 -0.06958578 0.087762035 0.049649521 -0.104057987 -0.05858629 -0.009131051 -0.000649269 -0.24294753 -0.0257553 0.071610895 -0.037340619 -0.020100429 -0.043907076 0.085736184 0.089969474 -0.032084298 0.012482425 0.074145353 0.104939786 0.02153867 -0.007406289 -0.01550563 0.061175265 -0.026331117 0.054859677 0.016874486 -0.094693853 0.018536813 -0.019755718

19/08/2010

356.9

2690.81

19/09/2010

385.4

2844.71

19/10/2010

383.1

2947.99

19/11/2010

366.8

2959.82

19/12/2010

372.1

3044.15

19/01/2011

380.8

3103.83

19/02/2011

384

3154.1

19/03/2011

351

2973.64

0.030312 0.079854 -0.00597 -0.04255 0.014449 0.023381 0.008403 -0.08594

0.012324825 0.057194674 0.036305985 0.004012904 0.028491597 0.019604816 0.016196119 -0.057214419

APPENDIX 1.3b REGRESSIONANALYSIS SUMMARY OUTPUT Regression Statistics Multiple R 0.393155 R Square 0.154571 Adjusted R Square 0.151625 Standard Error 0.07044 Observations 289 ANOVA

Regression Residual Total

Intercept X Variable 1

Significance df SS MS F F 1 0.260358339 0.260358 52.47244 4.03E-12 287 1.424039673 0.004962 288 1.684398012 Standard Coefficients Error t Stat P-value 0.001231 0.004166711 0.295457 0.767858 0.618599 0.085397227 7.243787 4.03E-12

Upper Lower 95% 95% -0.00697 0.009432 0.450515 0.786684

Lower 95.0% -0.00697 0.450515

Rf (given)

equity beta x Mkt risk

Calculation: cost of equity, ke CAPM

4.20% ke

equity beta 0.618599293

Mkt risk 0.0546

0.033776

7.58% Share Price 19th 2011

Issued Shares £3.51

1872millions

Market value of ordinary shares: £351x1872 million = £6570.72 million Net financial obligation

= £ 2215 million

Upper 95.0% 0.009432 0.786684

APPENDIX 2.1 COMMON SIZE AND TREND ANALYSIS FOR SAINSBURY’S IN PERCENTAGE 2008 £m

2008 £m

2009 £m

2009 £m

2010 £m

2010 £m

2011 £m

2011 £m

Operating Income 100

Revenue Cost of sales

-0.94

istrative Expenses Operating Income from Sales (before tax)

-0.03

Tax on Ordinary Activities

106.0212 -94.52

-0.97

-2.22

99.03

111.9247 -94.5802

-96.7426

-2.00

3.257363

118.3046 -94.5029

-96.5788

-1.98

3.42

3.52

-0.01

-0.94

-0.74

-0.89

Tax on Other Income

0.00

0.08

0.04

0.14

Tax on Financial Items

0.00

-0.14

-0.16

-0.11

Total Operating Tax Operating Income from Sales (After tax) Other Operating Income (before tax)

-0.01

-0.99

-0.86

-0.85

0.02

-0.01

0.00

0.00

Other Income

0.00

0.30

0.14

0.51

Less: Tax Share of Post-Tax loss from t Ventures Other Operating Income (After tax) Dirty Surplus Items of Operating Activities Actuarial gains on defined benefit pension schemes Less Tax impact on above item

0.00

-0.08

-0.04

-0.14

0.00

-0.59

0.69

0.28

Operating Income

-96.479

0.00

-0.37

0.79

0.65

0.03

-4.77

-0.87

0.14

-0.01

1.34

0.24

-0.01

0.04

-3.81

0.16

0.77

Less: Financing expense (income): Finance expense

-0.01

-0.78

-0.74

-0.54971

Finance Income

0.00

0.27

0.17

0.15

0.00

-0.51

-0.58

-0.40

0.00

0.14

0.16

0.11

Less: Tax benefit

0.00

-0.36

-0.41

-0.29

Dirty Surplus Items of Financial Activities: Available-for-sale financial assets: Group Available-for-sale financial assets: t ventures Cash flow hedge: Group

0.00

-0.08

0.22

0.07

0.00

-

0.00

0.05

Cash flow hedge: t Venture

0.00

-0.17

Share based payment Less: Tax on the above components of other comprehensive income Comprehensive Income to Ordinary Shareholders

0.00 0.00

0.00

0.02

-0.5

0.12

0.01

-0.02

-0.04

-

0.01

-

-

-0.06

-0.15

-0.01

-0.25

0.04

-2.1

2.57

3.19

0.04

-2.1

2.57

3.19

APPENDIX 2.2a SAINSBURYS REFORMATED INCOME STATEMENT FOR THE PERIODS 2008 – 2011 2008

2008

2009

2009

2010

2010

2011

2011

£m

£m

£m

£m

£m

£m

£m

£m

Operating Income Revenue Cost of sales istrative Expenses

17837 -16835 -502

Operating Income from Sales (before tax) Tax on Ordinary Activities Tax on Other Income Tax on Financial Items

18911 -17875

-17337

-420

500

19964 -18882

-18295

-399

616

21102 -19942

-19281

-417

683

743

-150

-177

-148

-187

9

16.074

7.56

30.24

-14.7

-27.072

-32.2

-23.52

Total Operating Tax Operating Income from Sales (After tax)

-20359

-155.7

-187.998

-172.64

-180.28

344.3

428.002

510.36

562.72

Other Operating Income (before tax) Other Income

30

57

27

108

Less: Tax

-9

-16.074

-7.56

-30.24

Share of Post-Tax loss from t Ventures Other Operating Income (After tax)

-2

-111

138

60

Dirty Surplus Items of Operating Activities Actuarial gains on defined benefit pension schemes Less Tax impact on above item Operating Income

19

-70.074

157.44

137.76

542

-903

-173

29

-151

253

48

-3

754.3

-292.072

542.8

726.48

Less: Financing expense (income): Finance expense Finance Income Less: Tax benefit

-132

-148

-148

83

52

33

-116

-49

-96

-115

-84

14.7

27.072

32.2

23.52

-34.3

-68.928

-82.8

-60.48

-31

-16

43

14

24

2

-3

-8

32

Dirty Surplus Items of Financial Activities: Available-for-sale financial assets: Group Available-for-sale financial assets: t ventures Cash flow hedge: Group

-

48 2

Cash flow hedge: t Venture

-58

Share based payment Less: Tax on the above components of other comprehensive income Total Comprehensive Income(to Ordinary Shareholders)

-10 -1

9 -

-32 -84.3

2

4

-103.928

-11

-29.8

-3

-53.48

670

-396

513

673

670

-396

513

673

APPENDIX 2.2b TESCO'S REFORMATED INCOME STATEMENT FOR THE PERIODS 2008 – 2011 2008

2008

2009

2009

2010

2010

2011

2011

£m

£m

£m

£m

£m

£m

£m

£m

Operating Income Revenue Cost of sales istrative Expenses

47298

54327

56910

60931

-43668

-50109

-52303

-55871

-1027

-1248

-1527

-1676

Operating Income from Sales (before tax)

-44695

-51357

-53830

-57547

2603

2970

3080

3384

Tax on Ordinary Activities

-673

-788

-840

-864

Tax on Other Income

56.4

105.56

119.56

Tax on Financial Items

-18.9

66.55 102.08

Total Operating Tax Operating Income from Sales (After tax)

-87.92

-93.24

-635.5

-823.53

-822.36

-837.68

1967.5

2146.47

2257.6

2546.32

Other Operating Income (before tax) Profit arising from Property-related items Less: Tax

188

236

377

427

-56.4

-66.55

-105.56

-119.6

Loss from operating activities Share of post-tax profits of t ventures and associates Other Operating Income (After tax)

75

110

33

57

206.6

279.45

304.44

364.44

38

-275

343

-344

187

-629

-322

595

54

-153

Dirty Surplus Items of Operating activities Foreign currency translation differences Total gain/Loss on defined benefit pension scheme Tax relating to Components of other C.Income Tax on item taken directly to equity

123

Total Other operating Income Operating Income

435 554.6

-189.55

379.44

462.44

2522.1

1956.92

2637.1

3008.76

Less: Financial Expense Finance cost Finance Income Less: Tax

-250

-478

-579

-483

187

116

265

150

-63

-362

-314

-333

18.9

-44.1

102.08

33

-259.92

87.92

-226.08

93.24

-239.76

Dirty Surplus Items of Financing activities Change/Loss on revaluation of available-for-sale investments Reclassified and reported in Group Income Statement

-4

3

1

-29

5

Fair value Movements of Cash flow hedges

66

-334 505

Total Comprehensive Income Minority Interest Comprehensive Income to ordinary shareholders

174

-168

2 8 -162

-22

-12

2511

1871

2249

2757

-11

-1

-27

-11

2500

1870

2222

2746

APPENDIX 2.3a SAINSBURY’S REFORMULATED GROUP BALANCE SHEET FOR THE PERIOD 2009-2012

2008 £m

2008

2009 £m

£m

2009 £m

2010 £m

2010 £m

2011 £m

2011 £m

Operating Assets (OA) Property Plant and Machinery

7424

7821

8203

8784

Intangible Assets

165

160

144

151

Investment in t Venture

148

288

449

502

55

45

36

36

Other Receivables Retirement Benefit Assets

495

Inventories

681

-

-

Non-current assets held for sale

112

21

56

13

Trade and Other Receivables

206

195

215

343

Cash and cash equivalents

719

689

10005

627

702

9846

837

812

10642

501

11142

Less: Operating Liabilities (OL) Trade and other payables

2280

2488

2466

2597

Current Provisions

10

19

13

11

Non-current Provisions

63

57

66

62

Taxes Payable

191

202

200

201

Other Payables

89

92

106

120

321

95

144

172

Deferred income tax liability Retirement benefit obligation

-

2954

Net Operating Assets(NOA)

309

7051

3262

421

6584

3416

340

7226

3503 7639

Financial Assets (FA) Available for Sales Non-current derivative financial instruments Current derivative financial instruments

Less: Financial Obligations (FO) Current Derivatives Financial Instrument liabilities Non-Current Derivatives Financial Instrument liabilities Borrowings: amount falling due within 1 year Borrowings: amount falling due after more than 1 year

106 4

97

150

176

31

20

29

59

43 187

213

257

7161

6771

7439

7896

6

56

41

18

8

2

118

154

73

2084

52

110

2226

Net Financial Obligations (NFO)

2116

Non- Controlling Interest (NCI)

-

Common Shareholders' Equity (CSE)

4935

2177

2395 2208 4376

2357

59 74 2473

2339

2472

2260

2215

-

-

4966

5424

APPENDIX 2.3b TESCO PLC REFORMULATED GROUP BALANCE SHEET 2008 2008 £m £m Operating Assets (OA) Goodwill and other Intangible Assets Property, Plant and Equipment Investment Property Investment in t Ventures and Associates Other Investments Deferred tax assets Inventories Trade and Other Receivables Current Tax Assets Cash Less: Operating Liabilities (OL) Trade and other payables Customer Deposits Current Tax liabilities Non-current Provision Current Provision Post-employment benefit Obligation Deferred tax Liabilities Other non-current payables Deposits by banks Net Operating Assets (NOA) Financial Assets (FA) Non-Current Derivative Financial InstrumentsAssets Current Derivative Financial InstrumentsAssets Non-Current Loans and Advances to customers Current Loans and Advances to customers Current Loans and Advances to banks and other financial assets Short-term Investments Cash and Cash equivalents Non-current assets classified as held for sale Less: Financial Obligations Borrowings: amount falling due within 1 year Borrowings: amount falling due after more than 1 year Current Derivative Financial Instruments- and other Liabilities Liabilities of the disposal group classified as held for sale Non-Current Derivative Financial Instrumentsand other Liabilities Net Financial Obligation (NFO) Non-Controlling Interests Common Shareholders' Equity (CSE)

2336 19787 1112 305 4 104 2430 1311 6 1542

28937

7277 455 23 4 838 802 42 9441 19496

2009 2009 2010 2010 £m £m £m £m 4027 23152 1539 62 259 21 2669 1798 9 2112

8522 4538 362 67 10 1494 696 68 24

35648

15781 19867

4177 24203 1731 152 863 38 2729 1888 6 2062

9442 4357 472 172 39 1840 795 30

37849

17147 20702

2011 2011 £m £m 4338 24398 1863 316 1108 48 3162 2314 4 1785

10484 5074 432 113 64 1356 1094 36

216

1478

1250

1139

97

382 1470 1918

224 1844 2268

148 2127 2514

2129 1233 1397 398

144 1314 757 373

404 1022 85 431

360 246 308

1227 20723

10405 30272

8174 28876

2084

4059

1529

1386

5972

12391

11744

9689

443

525

146

255

-

-

322

8821 11902 87 11815

302

17277 12995 57 12938

776

14195 14681 85 14596

600

39336

18653 20683

7870 28553

11930 16623 88 16535

APPENDIX 3.1a SAINSBURY'S REFORMATED CASHFLOW STATEMENT FOR THE PERIODS 2008- 2011 2008 £m

2008

2009

£m

£m

2009

2010

£m

£m

2010

2011

£m

£m

2011 £m

Cash from Operating Activities ( C ) Cash generated from operations Corporation Tax paid Tax on Interest

998

1206

-64 -28.2

1206

-160 -92.2

Dividend Received

-

-32.43

-89 -192.43

905.8

3

905.8

Cash Investments (I) Acquisition of and investment in Subsidiaries

1138

-26.04

-158 -115.04

1016.57

-28.89

2

-186.89

1092.96

1016.57

1

1092.96

952.11

-7

-10

-973

-966

-1036

-1136

Proceeds from disposal of PPE & other Assets

198

390

139

282

Proceeds from Sale of Intangible Asset

-

-

Purchase of PPE

Purchase of intangible assets

-6

Invested in t ventures and associates

-31

Cost of disposal of Operations

-1

Free Cash Flow C - I

-

-

-15

-2 -887

85.8

-

-11

-291 -820

-1

-10

952.11

-

129.57

-2 -910

-872

182.96

80.11

Financial Flow to Claimants (F) Interest Paid

123

128

111

126

Interest Received

-29

-13

-18

-19

94

115

93

107

Tax On Interest

-28.2

65.8

Investment in Financial Assets

-

Repayments of Long-term Borrowing

-32.43

82.57

36

30

74

61

3

3

3

4

2

3

-235

-45

Proceeds from Long-term borrowing

-

-152

Proceeds from Short-term borrowing

-

-43

Repayments of Short-term Borrowing

-164

Total Debt Financing

-43

Dividends Paid

178

-

-59.2

-2

-73.43

145 85.8

235

-73.43

-15

10

36

-59.2

Equity Financing (d) Proceeds from Issuance of ordinary shares

Total Financing Flow (F+d)

78.11 50

-

Total Equity Financing

-28.89

10

-

Capital Redemption

66.96

8

Interest elements of Obligations under Finance Leases payments Repayment of capital element of obligations under finance lease payment

Increase/Decrease in Cash

-26.04

11 191.96

-334

191.96

-171.89

-250

218

241

-

-

-17 269 -

203 129.57

-171.89

-9 182.96

252 80.11

APPENDIX 3.1b TESCO'S REFORMATED CASHFLOW STATEMENT FOR THE PERIODS 2008- 2011 2008 £m

2008 £m

2009 £m

2009

2010 £m

£m

2010 £m

2011 £m

2011 £m

Cash from Operating Activities ( C ) Cash generated from operations

4099

Corporation Tax paid

-346

Tax on Interest

-84.6

Dividend Received Effect of foreign exchange rate changes

4978

5947

-456 -430.6

-133.104

-589.104

88 -55

5366

-512 -170.52

-760 -682.52

69 3701.4

120

3701.4

-136.08

-896.08

35 4577.896

49

4577.896

62 5348.48

-46

5348.48

4485.92 4485.92

Cash Investments (I) Acquisition of Subsidiaries Proceeds from sale of t ventures and associates

-169

-1275

-

Proceeds from sale of subsidiary

-

Purchase of PPE and Investment Property Proceeds from sale of PPE Proceeds from Sale of Intangible Asset

-

-

-

-

-

-

-4487

-2855

-3178

1056

994

1820

1906

4

3

-220

-163

-373

-

-158

Invested in t ventures and associates

-61

Free Cash Flow C - I

-2774

-30

927.4

Financial Flow to Claimants (F) Increase in loans to t ventures

-89

-3442 -

Purchase of intangible assets

-65

-5018

-4

-440.104

-1263

-174

4085.48

36

242

45

219

360 -

1233

1918

1264

Decrease in loans to t ventures

-25

Investments in short-term investments Proceeds from sale of short-term Investments Interest Paid Interest Received Tax On Interest Increase in borrowings Repayments of Borrowing New Finance Leases Repayments of Obligations under Finance Leases Increase/Decrease in Cash

-360

410

-1233

562

-1314

690

614

-128

-90

-81

-128

282

472

609

486

-84.6

197.4

-133.104

338.896

-170.52

438.48

-136.08

349.92

-9333

-7387

-862

-2175

7593

2733 -

3601

4153

-119 32 746

Total Debt Financing Equity Financing (d) Ordinary shares issued for cash

-

18 -487.6

1721

-487.6

-138

41

-1461.104

-690

-1461.104

42 3258.48

-949

3258.48

-130

-167

-

-

-98

-16

Dividends Paid

792

883

968

1081

2

3

2

2

Own Shares Purchased Other Adjustments Total Equity Financing Total Financing Flow (F+d)

775 -

265

-

24

-

1564.92 1564.92

Proceeds from sale of ordinary share capital to minority interests Dividends Paid to Minority Interest

-1905 2580.92

31

-

-

1415

1021

827

1016

927.4

-440.104

4085.48

2580.92

APPENDIX 3.2a ANALYST FORECAST AND MY PREDICTIONS RBS

Evolution Security PLC

Own Outcome

Santander

2012

2012

2012

2012

2012

2012

2012

2012

£m

£m

£m

£m

£m

£m

£m

£m

Operating Income Revenue

22540

Cost of sales

22085

-21301

istrative Expenses Operating Income from Sales (before tax)

-445.417

Tax on Ordinary Activities

-199.743

-21746.368

-436.425

793.63

Tax on Other Income Tax on Financial Items

22325.6

-20871

22007.67

-21098.3 -21307.3886

-441.18

777.61

-20797.88 -21539.52

-434.90

786.08

-195.711

774.89

-197.843

-195.03

29.99

29.39

29.71

29.29

-23.3283

-22.8574

-23.11

-22.78

Total Operating Tax Operating Income from Sales (After tax)

-21232.78

-193.08

-189.18

-191.24

-188.52

600.55

588.43

594.84

586.37

Other Operating Income (before tax) Other Income Less: Tax Share of Post-Tax loss from t Ventures

115.3597

113.031

114.2624

112.64

-29.99

-29.39

-29.71

-29.29

64.09

62.79

63.48

62.58

Other Operating Income (After tax) Dirty Surplus Items of Operating Activities Actuarial gains on defined benefit pension schemes Less Tax impact on above item Operating Income

149.45

146.44

148.03

145.93

30.98

30.35

30.68

30.24

8.05

7.89

7.98

7.86

789.04

773.11

781.53

770.40

Less: Financing expense (income): Finance expense Finance Income

Less: Tax benefit Dirty Surplus Items of Financial Activities: Available-for-sale financial assets: Group Available-for-sale financial assets: t ventures Cash flow hedge: Group Cash flow hedge: t Venture Share based payment Less: Tax on the above components of other comprehensive income Total Comprehensive Income(to Ordinary Shareholders)

-123.905

-121.404

-122.73

-120.98

34.18

33.49

33.86

33.37

-89.72

-87.91

-88.87

-87.61

23.33

22.86

23.11

22.78

-66.40

-65.06

-65.76

-64.83

14.95

14.65

14.81

14.60

2.14

2.09

2.12

2.09

-8.55

-8.37

-8.46

-8.34

2.14

2.09

-

2.12

2.78

-52.94

2.09

2.72

-51.87

2.75

-52.43

-3.13

-57.53

736.10

721.24

729.10

712.88

736.10

721.24

729.10

712.88

APPENDIX 3.2b SAINSBURY’S 2012 ACTUAL OUTCOME ACTUAL OUTCOMES 2012 2012 £m £m Operating Income 22294

Revenue

-21083 -419

Cost of sales istrative Expenses

Operating Income from Sales (before tax)

-21502 792

-201 21.32 -26.78

Tax on Ordinary Activities Tax on Other Income Tax on Financial Items

-206.46 585.54

Total Operating Tax

Operating Income from Sales (After tax) Other Operating Income (before tax) 82 -21.32 28

Other Income Less: Tax Share of Post-Tax loss from t Ventures

Other Operating Income (After tax) Dirty Surplus Items of Operating Activities

88.68

Actuarial gains on defined benefit pension schemes

-222 68 520.22

Less Tax impact on above item

Operating Income Less: Financing expense (income): Finance expense

-138 35 -103 26.78 -76.22

Finance Income Less: Tax benefit

Dirty Surplus Items of Financial Activities: Available-for-sale financial assets: Group

1 2

Available-for-sale financial assets: t ventures Cash flow hedge: Group

-

Cash flow hedge: t Venture Share based payment Less: Tax on the above components of other comprehensive income

Total Comprehensive Income(to Ordinary Shareholders)

2 2

-69.22 451 451

APPENDIX 4.1a Ratio analysis for Sainsbury's: Ratios (Level 3)

2008

Asset Turnover (ATO) Drivers: PPE Turnover Inventory Turnover Receivable Turnover Other Asset Turnover Payable Turnover Other Liabilities Turnover 1/ATO

2009

0.42 0.04 0.01 0.09 0.13 0.04 0.40

0.41 0.04 0.01 0.06 0.13 0.04 0.35

2010

0.41 0.04 0.01 0.08 0.12 0.05 0.36

2011

0.42 0.04 0.02 0.06 0.12 0.04 0.36

APPENDIX 4.1b Ratio analysis for TESCO PLC: Ratios (Level 3)

2008

2009

2010

2011

Asset Turnover (ATO) Drivers:

PPE Turnover Inventory Turnover s Receivable Turnover Other Assets Turnover s Payable Turnover Other Liability Turnover 1/ATO

0.42 0.05 0.03 0.12 0.15 0.05 0.41

0.43 0.05 0.03 0.26 0.16 0.14 0.47

0.43 0.05 0.03 0.24 0.17 0.15 0.44

0.40 0.05 0.04 0.25 0.17 0.14 0.42

12 January 2011

Price/Target:

390p/350p

Mkt Cap:

£7,470m

Net Cash/(Debt) (FY1)

Mar

2010A

PBT EPS (p) DPS (p) P/E (x)

-£2,706m

2011E

2012E

610

654

727

23.3

25.1

27.0

14.2

15.3

16.6

16.8x

15.5x

14.4x

600

Sainsburys

Reduce

(SBRY.L)

What lies beneath On the surface, headline Q3 LFL sales growth of 3.6% appears attractive. But, the underlying figures are much less impressive, reflect the industry slowdown and suggest that momentum is slowing. Most noticeably, the substantial extension program and last January’s VAT rise are clouding the underlying trends. Stripping out these impacts, reported 3.6% expetrol LFLs would fall to c1.5%, suggesting flattish volumes. With underlying growth unimpressive, margin expansion limited and the industry outlook deteriorating, we see no reason why Sainsbury’s should command a 20% 2012 PE to the sector. We urge caution and rate the stock a Reduce with a 350p target price.

550 500 450 400 350 300 250 200 Jan 06 Jul 06 Jan 07 Jul 07 Jan 08 Jul 08 Jan 09 Jul 09 Jan 10 Jul 10 Jan 11 Source: FactSet Estimates

Price

Price Relative to FTSE 100

Results: Sainsbury’s delivered total sales growth of +7.5% slightly shy of our +8% estimate. Excluding petrol, total sales growth of 6.0% was also a touch behind our 6.5% forecast. LFLs of +3.6% were broadly in line. Although 3.6% headline growth appears higher than Morrisons 1%, we note that on the same definition, the growth rates are broadly similar.

Extension impact: With over 300k sq ft of extensions in this quarter (550k year to date), the underlying LFL picture is clouded by the inclusion of this additional space in LFLs. Sainsbury’s explained this extra space contributed c1% to growth. Last quarter extensions contributed 0.3% to LFL sales and going forward the impact will be even greater than the c1% reported today.

Industry outlook: Management were unequivocal in explaining the pervasive impact of inflation and on their concerns for the consumer outlook. They echoed Kantar in talking about a boost to non-food sales over Christmas as consumers moved away from the High Street due to accessibility and the adverse weather. This shift could cloud the underlying picture and see January sales disappoint as consumers revert back to the High Street.