Cost ing Cycle 3j6o5w

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report r6l17

Overview 4q3b3c

& View Cost ing Cycle as PDF for free.

More details 26j3b

- Words: 631

- Pages: 4

Cost Concepts

Cost Cycle

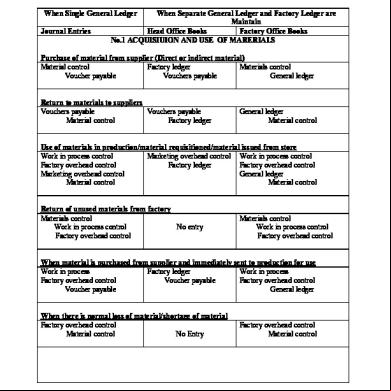

Cost ing Cycle When Single General Ledger Journal Entries

When Separate General Ledger and Factory Ledger are Maintain Head Office Books Factory Office Books No.1 ACQUISIUION AND USE OF MARERIALS

Purchase of material from supplier (Direct or indirect material) Material control Factory ledger Materials control Voucher payable Vouchers payable General ledger Return to materials to suppliers Vouchers payable Vouchers payable Material control Factory ledger

General ledger Material control

Use of materials in production/material requisitioned/material issued from store Work in process control Marketing overhead control Work in process control Factory overhead control Factory ledger Factory overhead control Marketing overhead control General ledger Material control Material control Return of unused materials from factory Materials control Work in process control No entry Factory overhead control

Materials control Work in process control Factory overhead control

When material is purchased from supplier and immediately sent to production for use Work in process Factory ledger Work in process Factory overhead control Voucher payable Factory overhead control Voucher payable General ledger When there is normal loss of material/shortage of material Factory overhead control Material control No Entry

Composed by: Baber Mehmood

Factory overhead control Material control

Cost Concepts

Cost Cycle No.2 USE OF LABOUR

Recording gross payroll, deductions and net pay Payroll Payroll Income tax withheld Income tax withheld Provident fund payable Provident fund payable Any other deduction Any other deduction Accrued payroll Accrued payroll

No Entry

Preparing payroll voucher and payment Accrued payroll Accrued payroll Vouchers payable Vouchers payable

No entry

Payment of voucher Vouchers payable Cash

No entry

Distribution of payroll Work in process control Factory overhead control Selling overhead control n. overhead control Payroll control

Vouchers payable Cash Factory ledger Marketing overhead control n. Overhead control Payroll control

Work in process control Factory overhead control General ledger

Recording employer’s liability for contribution Factory overhead control Selling overhead control n. Overhead control Provident fund payable Social security payable

Factory ledger Marketing overhead control n. Overhead control Provident fund payable Social security payable

Factory overhead control General ledger

No.3 INSURANCE AND CHARGE OF FACTORY OVERHEAD Recording actual factory overhead Factory overhead actual Factory overhead actual Utilities payable Utilities payable Prepaid insurance Prepaid insurance Allowance for dep. Allowance for dep. OR OR Voucher payable Voucher payable Charged of FOH applied to production Work in process Factory overhead applied

Composed by: Baber Mehmood

No entry

Factory overhead control General ledger

Work in process FOH applied

Cost Concepts

Cost Cycle

Close FOH applied to FOH control A/c FOH applied FOH control

No entry

To record FOH Under-applied Cost of goods sold Under applied FOH

General ledger Under applied FOH

OR WIP-Material WIP-Labour WIP-FOH Finished goods Cost of goods sold Under applied FOH

FOH applied FOH control

Cost of goods sold Factory ledger

To close under applied FOH to FOH control a/c Under applied FOH No entry FOH control

OR WIP-Material WIP-Labour WIP-FOH Finished goods General ledger Under applied FOH

Under applied FOH FOH control

No.4 TRANSFER OF COST TO FINISHED GOODS When one WIP a/c is issued Finished goods control Work in process

No entry

When three WIP a/c are used Finished goods control WIP-Material WIP-Labour WIP-FOH

Finished goods control Work in process

No entry

No. 5 SALE OF FINISHED GOODS To record cost of goods sold Cost of goods sold control Finished goods control

Cost of goods sold control Factory ledger

General ledger Finished goods control

To Record Return of Goods at Cost Finished goods control Cost of goods sold control

Factory ledger Cost of goods sold control

Composed by: Baber Mehmood

Finished goods control General ledger

Cost Concepts

Cost Cycle

To Record Sale Price Cash receivable Sale control

Cash receivable Sale control

To Record Sale Return Sale return s receivable

Sale return s receivable

Composed by: Baber Mehmood

No entry

No entry

Cost Cycle

Cost ing Cycle When Single General Ledger Journal Entries

When Separate General Ledger and Factory Ledger are Maintain Head Office Books Factory Office Books No.1 ACQUISIUION AND USE OF MARERIALS

Purchase of material from supplier (Direct or indirect material) Material control Factory ledger Materials control Voucher payable Vouchers payable General ledger Return to materials to suppliers Vouchers payable Vouchers payable Material control Factory ledger

General ledger Material control

Use of materials in production/material requisitioned/material issued from store Work in process control Marketing overhead control Work in process control Factory overhead control Factory ledger Factory overhead control Marketing overhead control General ledger Material control Material control Return of unused materials from factory Materials control Work in process control No entry Factory overhead control

Materials control Work in process control Factory overhead control

When material is purchased from supplier and immediately sent to production for use Work in process Factory ledger Work in process Factory overhead control Voucher payable Factory overhead control Voucher payable General ledger When there is normal loss of material/shortage of material Factory overhead control Material control No Entry

Composed by: Baber Mehmood

Factory overhead control Material control

Cost Concepts

Cost Cycle No.2 USE OF LABOUR

Recording gross payroll, deductions and net pay Payroll Payroll Income tax withheld Income tax withheld Provident fund payable Provident fund payable Any other deduction Any other deduction Accrued payroll Accrued payroll

No Entry

Preparing payroll voucher and payment Accrued payroll Accrued payroll Vouchers payable Vouchers payable

No entry

Payment of voucher Vouchers payable Cash

No entry

Distribution of payroll Work in process control Factory overhead control Selling overhead control n. overhead control Payroll control

Vouchers payable Cash Factory ledger Marketing overhead control n. Overhead control Payroll control

Work in process control Factory overhead control General ledger

Recording employer’s liability for contribution Factory overhead control Selling overhead control n. Overhead control Provident fund payable Social security payable

Factory ledger Marketing overhead control n. Overhead control Provident fund payable Social security payable

Factory overhead control General ledger

No.3 INSURANCE AND CHARGE OF FACTORY OVERHEAD Recording actual factory overhead Factory overhead actual Factory overhead actual Utilities payable Utilities payable Prepaid insurance Prepaid insurance Allowance for dep. Allowance for dep. OR OR Voucher payable Voucher payable Charged of FOH applied to production Work in process Factory overhead applied

Composed by: Baber Mehmood

No entry

Factory overhead control General ledger

Work in process FOH applied

Cost Concepts

Cost Cycle

Close FOH applied to FOH control A/c FOH applied FOH control

No entry

To record FOH Under-applied Cost of goods sold Under applied FOH

General ledger Under applied FOH

OR WIP-Material WIP-Labour WIP-FOH Finished goods Cost of goods sold Under applied FOH

FOH applied FOH control

Cost of goods sold Factory ledger

To close under applied FOH to FOH control a/c Under applied FOH No entry FOH control

OR WIP-Material WIP-Labour WIP-FOH Finished goods General ledger Under applied FOH

Under applied FOH FOH control

No.4 TRANSFER OF COST TO FINISHED GOODS When one WIP a/c is issued Finished goods control Work in process

No entry

When three WIP a/c are used Finished goods control WIP-Material WIP-Labour WIP-FOH

Finished goods control Work in process

No entry

No. 5 SALE OF FINISHED GOODS To record cost of goods sold Cost of goods sold control Finished goods control

Cost of goods sold control Factory ledger

General ledger Finished goods control

To Record Return of Goods at Cost Finished goods control Cost of goods sold control

Factory ledger Cost of goods sold control

Composed by: Baber Mehmood

Finished goods control General ledger

Cost Concepts

Cost Cycle

To Record Sale Price Cash receivable Sale control

Cash receivable Sale control

To Record Sale Return Sale return s receivable

Sale return s receivable

Composed by: Baber Mehmood

No entry

No entry

Related Documents 171j1w

Cost ing Cycle 3j6o5w

November 2019 73

4-the Cost ing Cycle 583i39

November 2019 41

Cost ing 5tgr

December 2019 188

Cost ing 5tgr

December 2021 0

Cost ing 5tgr

January 2021 0

Cost ing 5tgr

June 2020 5More Documents from "M Ali Mustafa" 5t3g1i

Cost ing Cycle 3j6o5w

November 2019 73

Nsn Ultra Bts Commissioning Report 5x286j

October 2019 40

Penyakit Siflis Esei 6z4i3f

January 2021 0

Manase-relax-please-part-1.pdf 5s466d

November 2019 36

Lubricant And Lubrication Fundamentals d581y

October 2022 0