Financial System And Financial Market 4z1j71

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report r6l17

Overview 4q3b3c

& View Financial System And Financial Market as PDF for free.

More details 26j3b

- Words: 2,990

- Pages: 10

NPTEL Course Course Title: Security Analysis and Portfolio Management Course Coordinator: Dr. Jitendra Mahakud

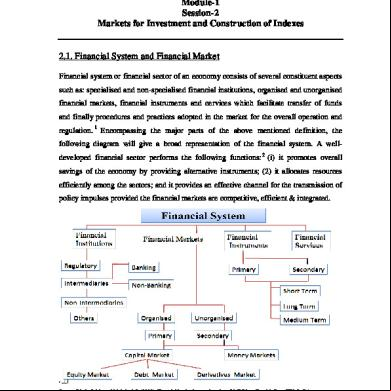

Module-1 Session-2 Markets for Investment and Construction of Indexes

2.1. Financial System and Financial Market Financial system or financial sector of an economy consists of several constituent aspects such as: specialised and non-specialised financial institutions, organised and unorganised financial markets, financial instruments and cervices which facilitate transfer of funds and finally procedures and practices adopted in the market for the overall operation and regulation. 1 Encoming the major parts of the above mentioned definition, the following diagram will give a broad representation of the financial system. A welldeveloped financial sector performs the following functions: 2 (i) it promotes overall savings of the economy by providing alternative instruments; (2) it allocates resources efficiently among the sectors; and it provides an effective channel for the transmission of policy impulses provided the financial markets are competitive, efficient & integrated.

Source: Bhole, L.M., and Mahakud, J. (2009), Financial institutions and markets.5th Edition, Tata McGraw Hill (India)

1

Bhole, L.M., and Mahakud, J. (2009), Financial institutions and markets.5th Edition, Tata McGraw Hill (India).

2

1

In a more theoretical sense financial markets can be defined as the centers or arrangements that provide facilities for demand and supply side of financial claims and services. The primary role of financial markets, broadly interpreted, is to intermediate resources from savers to investors, and allocates them in an efficient manner among competing uses in the economy, thereby contributing to growth both through increased investment and through enhanced efficiency in resource use.3 Classification of financial markets can be made on the basis of several aspects such as: (i) Nature of Claims (e.g., debt market, equity market); (2) Maturity of Claims (e.g., money market, capital market); (3) Seasoning of Claims (e.g., primary market, secondary market); (4) Timing of Delivery (e.g., cash or spot market, forward or futures market); (5) Organizational Structure (e.g., exchange traded market, over the counter market). The important characteristics of a good market for goods and services are as follows:4 1. Timely and accurate information: timely and accurate information is available on the price and volume of past transactions and the prevailing bid and ask prices. 2. Liquidity: an asset can be bought or sold quickly at a price close to the prices for previous transactions (has price continuity), assuming no new information has been received. In turn, price continuity requires depth. 3. Price continuity: prices do not change much from one transaction to the next unless substantial new information becomes available. 4. Depth: Presence of numerous potential buyers and sellers who are willing to trade at prices above and below the current market price. These buyers and sellers enter the market in response to changes in supply and demand or both and thereby prevent drastic price changes. 5. Low transaction cost: as transactions entail low costs, including the cost of reaching the market, the actual brokerage costs, and the cost of transferring the asset. 6. Informational efficiency: prices rapidly

3 4

Mohan Rakesh, (2007), Development of Financial Markets in India, RBI Monthly Bulletin Reilly, Frank. and Brown, Keith, “Investment Analysis & Portfolio Management”, 7th Edition, Thomson Soth-Western.

2

adjust to new information; thus, the prevailing price is fair because it reflects all available information regarding the asset. Financial markets are said to be perfect when, (i) a large number of savers and investors operate in markets, (ii) the savers and investors are rational, (iii) all operations in the markets are well informed and information is freely available to all of them, (iv) there are no transaction costs, (v) the financial assets are infinitely divisible, (vi) the participants in markets have homogeneous expectations, and (vii) there are no taxes. The equilibrium in financial markets is usually determined by assuming that there would be perfect competition, and by using the well known tool of supply and demand. Following the above mentioned ideal conditions, the financial market equilibrium position when the expected demand for funds (credit) for short-term and long-term investments matches with the planned supply of funds generated out of savings and credit creation. 5 Equilibrium is established when the expected demand for funds (credit) for short-term & long-term investment matches with the planned supply of funds generated out of savings and credit creation (Figure A,B &C ). Interest rate can also be fixed irrespective of the equilibrium rate of interest i.e. istered Interest rate (Figure D) in order to match/adjust supply and demand for funds as per economic policy requirement.

Source: Bhole, L.M., and Mahakud, J. (2009), Financial institutions and markets.5th Edition, Tata McGraw Hill (India)

5

Bhole, L.M., and Mahakud, J. (2009), Financial institutions and markets.5th Edition, Tata McGraw Hill (India).

3

2.1.1 Investment Decision, Alternative Markets and Asset Allocation An investment is the current commitment of dollars for a period of time in order to derive future payments that will compensate the investor for (1) the time the funds are committed, (2) the expected rate of inflation, and (3) the uncertainty of the future payments.6 In all cases, the investor is trading a known dollar amount today for some expected future stream of payments that will be greater than the current outlay. They invest to earn a return from savings due to their deferred consumption. The major investment characteristics of financial assets are, liquidity, marketability, reversibility, transferability, transaction costs, default risk, maturity period, tax status, buy-back options, price volatility and finally, the rate of return. Asset allocation is the process of deciding how to distribute an investor’s wealth among different countries and asset classes for investment purposes. An asset class is comprised of securities that have similar characteristics, attributes, and risk/return relationships.

The alternative financial assets under consideration for investment can be marketable and non-marketable assets. In case of marketable assets investor can manage and control the investment and subsequent liquidation process by his/her own decision. However these are less liquid in nature (e.g., all the market traded securities). In case of non-marketable assets although investor looses the day to day management but these are highly liquid (e.g., bank deposits, post office deposits etc.). The selected investment asset class may also be direct or indirect in of the ownership of the portfolio by the investor. In case of the direct financial assets investor owns the desired portfolio, whereas in case of indirect investor owns a portion of investment companies fund. 6

4

The broad range of financial markets that offer such financial assets can be categorised under the following four categories: In order to have a risk return trade-off Investors follow calculate the expected rate of return and evaluate the uncertainty, or risk, of an investment by identifying the range of possible returns from that investment and asg each possible return a weight based on the probability that it will occur. Most investors demand a higher rate of return on investments if they perceive that there is any uncertainty about the expected rate of return. The increase in the required rate of return over the zero risk return is called as the risk . Investors want a rate of return “investor’s required or expected rate of return” that compensates them for the time, the expected rate of inflation, and the uncertainty of the return. In a more formal way this risk is the uncertainty that an investment will earn its expected rate of return. Although the required risk for investing in a asset class represents a composite of all uncertainty, it is possible to consider several fundamental sources of uncertainty including: (a) business risk, (b) liquidity risk, (c) financial risk or leverage risk, (d) exchange rate risk, and (e) country (political) risk.

Source: Bhole, L.M., and Mahakud, J. (2009), Financial institutions and markets.5th Edition, Tata McGraw Hill (India)

The objective of maximising return can be pursued only at the cost of incurring higher risk. The financial markets offer a wide range of assets from very safe to very risky, with corresponding low to high returns. The above figure shows the risk return trade-off in a capital market line example. It shows the expected return risk spectrum

5

such that the representative asset classes are arrayed over a range of risk on it. The figure shows a positive linear relationship between expected return and risk for different set of asset classes. The rational risk averse investor will chose the appropriate investment opportunity by considering the desired level of risk.

2.2. Important Concepts Related to Capital Market 1. Margin Trading: This is the part of a transaction value that a customer has equity in the transaction. Use of Margin: to buy more, to borrow money. Concepts associated with margin: Initial margin: Amount Investor Puts up / value of transaction or It is the part of transaction’s value the customer must pay to initiate the transaction with other part being borrowed from the broker. Maintenance Margin: The percentage of a security’s value that must be on hand as equity. Margin Call: Demand from the broker for additional cash or securities as a result of the actual margin declining below the maintenance margin 2. Private Placement Vs. Preferential Allotment Private placements refer to sale of equity or equity related instruments of an unlisted company or sale of debentures of a listed or unlisted company. Preferential allotments refer to sale of equity or equity related instruments of an listed company. 3. Open Outcry Trading System: Under this system traders shout and resort to signals on the trading floor of the exchange which consists of several trading posts for different securities. Buyers make their bids and sellers make their offers and bargains are closed at mutually agreed-upon prices. 4. Screen-based Trading System: Started in November 4,1994 in India. The important features are: buyers and sellers place their orders on the computer. They can be limit order or best market price order. The computer constantly tries to match mutually compatible orders on price and time priority. The limit order book or the list of unmatched limit orders is displayed on the screen. Increases efficiency, confidence and transparency in the market

5. Settling: Electronic Delivery system and it is facilitated by depositories which is an institution which dematerializes physical certificates and effects transfer of ownership by electronic book entries. Example: National Securities Depository Limited (NSDL), Central Securities Depositories Limited (CSDL) 6. Settlement Procedure: Weekly Settlement, Carry forward system (badla and undha badla), Rolling Settlement (T+1).

6

7. Badla and Undha badla: When a bull buys in the anticipation of an immediate rise in price, but finds at the end of the ing period that the price has not risen, he may either pay for the shares and take delivery, or he may carry over his transaction to the next ing period by paying carry over charges or Seedha badla to the seller. When a bear sells in anticipation of a fall in prices in the immediate future (so that he can pick up shares later for delivery and make a profit), but the fall does not happen within the ing period, he has the option to borrow or buy the shares for delivery, or have his sales carried over to the next ing period on payment of Undha badla or backwardation charges to the buyer. 8. Short Selling: In a normal transaction a security is bought and owned because the investor believes the price is likely to rise. Eventually the security is sold and the position is closed out. First you buy then you sell. A short-sell involves selling a security because of belief that the price will decline and buying back the security later to close the position. First you sell and then buy. 9. Actual selling and buying procedure: Procedure for Buying - Locating the broker----Placement of order (De-mat in a depository) then - execution of order (Contract note for tax and other legal purposes). Order may be Limit Order (upper limit of the price has been given by the investor) or Market Order (to prevail the best market price).Procedure for selling- Placement of order-- sale order----- execution of order (same as buying) 10. Important abbreviations used in stock exchange quotations: Con-Convertible, Xd- ex (excluding) dividend, Cd- cum (with) dividend, Xr- ex(excluding) right.

2.3. Importance of Stock Market Index Three major advantage: to judge the performance of individual investor, to measure the market rates of return, to predict the market movements. Factors affecting the construction of stock market index: sample, it should be representative of total population, base year, it should be a normal year, weighting criteria, equally weighted series, price weighted series, market value weighted series. Example: Stock

Quantity

Beta

Price

A

60,000

30

45

B

20,000

25

80

C

90,000

65

85

7

Solution: Equally weighted series--1/3 (45/30 + 80/ 25 + 85 / 65) = 2.0033 Price weighted series--(45 + 80 + 85)/ )(30 + 25 + 65) = 1.75 Market value weighted series = (60 000*45 + 20 000*80 + 90 000* 85) / (60 000*30 + 20 000*25 + 90 000* 65) = 1.46 Popular Stock Market Indexes in India

_____________________________________________________________________

Additional Readings:

Alexander, Gordon, J., Sharpe, William, F. and Bailey, Jeffery, V., “Fundamentals of Investment, 3rd Edition, Pearson Education. Bodie, Z., Kane, A, Marcus,A.J., and Mohanty, P. “ Investments”, 6th Edition, Tata McGraw-Hill. Bhole, L.M., and Mahakud, J. (2009), Financial institutions and markets.5th Edition, Tata McGraw Hill (India).

Fisher D.E. and Jordan R.J., “Security Analysis and Portfolio Management”, 4th Edition., Prentice-Hall. Jones, Charles, P., “Investment Analysis and Management”, 9th Edition, John Wiley and Sons. Prasanna, C., “Investment Analysis and Portfolio Management”, 3rd Edition, Tata McGraw-Hill. Reilly, Frank. and Brown, Keith, “Investment Analysis & Portfolio Management”, 7th Edition, Thomson Soth-Western.

8

__________________________________________________________ Additional Questions with Answers Session 2: Markets for Investment and Construction of Indexes ______________________________________________________________________ 1. What are the different investment alternatives provided by different financial markets? Ans. Marketable and Non-Marketable Assets: • •

Marketable: Investor can manage and control, Less Liquid in Nature: All the Market Traded Securities Non-Marketable: No management but has Right, Highly Liquid: Bank Deposits, Post office Deposits, NSC etc.

Direct Vs. Indirect Investments: • •

Direct Investment: Investor—(owns)---Portfolio--- (Dividend and Interest)--Income and Capital gain Indirect Investments: Investor—(owns)---Investment Company’s Fund--(Dividend and Interest)---Income and Capital gain

Classification of Financial Markets: • Nature of Claims: Debt Market, Equity Market • Maturity of Claims: Money Market, Capital Market • Seasoning of Claims: Primary Market, Secondary Market • Timing of Delivery: Cash or Spot Market, Forward or Futures Market • Organizational Structure: Exchange Traded Market, Over the Counter Market • 2. What is the difference between Primary market and secondary market? Ans. Primary market • The primary market is that part of the capital markets that deals with the issuance of new securities. Primary market provides opportunity to issuers of securities, Government as well as corporate, to raise resources to meet their requirements of investment and/or discharge some obligation. • Equity Capital is raised in Primary Market. It can be raised through Public or primary Issue, Right Issue, Private Placement, Preferential Allotment • The primary market is governed by the provisions of the Companies Act, 1956, which deals with issues, listing and allotment of securities. Additionally the SEBI - prescribes the eligibility and disclosure norms to be complied by the issuer, promoter for accessing the market. Secondary Market • • •

Existing securities issued in the primary market are traded This market enables participants who held securities to adjust their holdings in response to changes in their assessment of risks and returns. It operates through over-the-counter (OTC) market and the exchange traded market. 9

• •

Operation of Secondary Market: Trading , Settlement Trading: Can be Open Outcry System and/or Screen-Based System. Under Open Outcry System traders shout and resort to signals on the trading floor of the exchange which consists of several trading posts for different securities. Buyers make their bids and sellers make their offers and bargains are closed at mutually agreed-upon prices. Under Screen-Based System Buyers and sellers place their orders on the computer. They can be limit order or best market price order. The computer constantly tries to match mutually compatible orders on price and time priority. • Modern settlement system is an electronic delivery mechanism: It is facilitated by Depositories which is an institution which dematerializes physical certificates and effects transfer of ownership by electronic book entries. Settlement Procedure can be Weekly Settlement, Carry forward system (badla and undha badla), Rolling Settlement (T+1) 3. What is the meaning of margin trading and what are the major concepts associated with it? Ans. • Margin Trading: This is the part of a transaction value that a customer has equity in the transaction. Use of Margin: to buy more, to borrow money Concepts associated with margin: •

• •

Initial margin: Amount Investor Puts up / value of transaction or It is the part of transaction’s value the customer must pay to initiate the transaction with other part being borrowed from the broker. Maintenance Margin: The percentage of a security’s value that must be on hand as equity. Margin Call: Demand from the broker for additional cash or securities as a result of the actual margin declining below the maintenance margin

4. Why stock market index is importance and what are the factors affecting construction of stock market index? Ans. A good Stock Index captures the movement of the well diversified and highly liquid stocks. It is the pulse rate of the economy. Index movements reflect the changing expectations of the stock market about future dividends of the corporate sector. Importance of Stock Market Index • To judge the performance of individual investor • To measure the market rates of return • To predict the market movements Factors affecting the construction of stock market index • Sample: It should be representative of total population • Base year: It should be a normal year • Weighting criteria – Equally Weighted Series – Price Weighted Series – Market value Weighted Series

10

Module-1 Session-2 Markets for Investment and Construction of Indexes

2.1. Financial System and Financial Market Financial system or financial sector of an economy consists of several constituent aspects such as: specialised and non-specialised financial institutions, organised and unorganised financial markets, financial instruments and cervices which facilitate transfer of funds and finally procedures and practices adopted in the market for the overall operation and regulation. 1 Encoming the major parts of the above mentioned definition, the following diagram will give a broad representation of the financial system. A welldeveloped financial sector performs the following functions: 2 (i) it promotes overall savings of the economy by providing alternative instruments; (2) it allocates resources efficiently among the sectors; and it provides an effective channel for the transmission of policy impulses provided the financial markets are competitive, efficient & integrated.

Source: Bhole, L.M., and Mahakud, J. (2009), Financial institutions and markets.5th Edition, Tata McGraw Hill (India)

1

Bhole, L.M., and Mahakud, J. (2009), Financial institutions and markets.5th Edition, Tata McGraw Hill (India).

2

1

In a more theoretical sense financial markets can be defined as the centers or arrangements that provide facilities for demand and supply side of financial claims and services. The primary role of financial markets, broadly interpreted, is to intermediate resources from savers to investors, and allocates them in an efficient manner among competing uses in the economy, thereby contributing to growth both through increased investment and through enhanced efficiency in resource use.3 Classification of financial markets can be made on the basis of several aspects such as: (i) Nature of Claims (e.g., debt market, equity market); (2) Maturity of Claims (e.g., money market, capital market); (3) Seasoning of Claims (e.g., primary market, secondary market); (4) Timing of Delivery (e.g., cash or spot market, forward or futures market); (5) Organizational Structure (e.g., exchange traded market, over the counter market). The important characteristics of a good market for goods and services are as follows:4 1. Timely and accurate information: timely and accurate information is available on the price and volume of past transactions and the prevailing bid and ask prices. 2. Liquidity: an asset can be bought or sold quickly at a price close to the prices for previous transactions (has price continuity), assuming no new information has been received. In turn, price continuity requires depth. 3. Price continuity: prices do not change much from one transaction to the next unless substantial new information becomes available. 4. Depth: Presence of numerous potential buyers and sellers who are willing to trade at prices above and below the current market price. These buyers and sellers enter the market in response to changes in supply and demand or both and thereby prevent drastic price changes. 5. Low transaction cost: as transactions entail low costs, including the cost of reaching the market, the actual brokerage costs, and the cost of transferring the asset. 6. Informational efficiency: prices rapidly

3 4

Mohan Rakesh, (2007), Development of Financial Markets in India, RBI Monthly Bulletin Reilly, Frank. and Brown, Keith, “Investment Analysis & Portfolio Management”, 7th Edition, Thomson Soth-Western.

2

adjust to new information; thus, the prevailing price is fair because it reflects all available information regarding the asset. Financial markets are said to be perfect when, (i) a large number of savers and investors operate in markets, (ii) the savers and investors are rational, (iii) all operations in the markets are well informed and information is freely available to all of them, (iv) there are no transaction costs, (v) the financial assets are infinitely divisible, (vi) the participants in markets have homogeneous expectations, and (vii) there are no taxes. The equilibrium in financial markets is usually determined by assuming that there would be perfect competition, and by using the well known tool of supply and demand. Following the above mentioned ideal conditions, the financial market equilibrium position when the expected demand for funds (credit) for short-term and long-term investments matches with the planned supply of funds generated out of savings and credit creation. 5 Equilibrium is established when the expected demand for funds (credit) for short-term & long-term investment matches with the planned supply of funds generated out of savings and credit creation (Figure A,B &C ). Interest rate can also be fixed irrespective of the equilibrium rate of interest i.e. istered Interest rate (Figure D) in order to match/adjust supply and demand for funds as per economic policy requirement.

Source: Bhole, L.M., and Mahakud, J. (2009), Financial institutions and markets.5th Edition, Tata McGraw Hill (India)

5

Bhole, L.M., and Mahakud, J. (2009), Financial institutions and markets.5th Edition, Tata McGraw Hill (India).

3

2.1.1 Investment Decision, Alternative Markets and Asset Allocation An investment is the current commitment of dollars for a period of time in order to derive future payments that will compensate the investor for (1) the time the funds are committed, (2) the expected rate of inflation, and (3) the uncertainty of the future payments.6 In all cases, the investor is trading a known dollar amount today for some expected future stream of payments that will be greater than the current outlay. They invest to earn a return from savings due to their deferred consumption. The major investment characteristics of financial assets are, liquidity, marketability, reversibility, transferability, transaction costs, default risk, maturity period, tax status, buy-back options, price volatility and finally, the rate of return. Asset allocation is the process of deciding how to distribute an investor’s wealth among different countries and asset classes for investment purposes. An asset class is comprised of securities that have similar characteristics, attributes, and risk/return relationships.

The alternative financial assets under consideration for investment can be marketable and non-marketable assets. In case of marketable assets investor can manage and control the investment and subsequent liquidation process by his/her own decision. However these are less liquid in nature (e.g., all the market traded securities). In case of non-marketable assets although investor looses the day to day management but these are highly liquid (e.g., bank deposits, post office deposits etc.). The selected investment asset class may also be direct or indirect in of the ownership of the portfolio by the investor. In case of the direct financial assets investor owns the desired portfolio, whereas in case of indirect investor owns a portion of investment companies fund. 6

4

The broad range of financial markets that offer such financial assets can be categorised under the following four categories: In order to have a risk return trade-off Investors follow calculate the expected rate of return and evaluate the uncertainty, or risk, of an investment by identifying the range of possible returns from that investment and asg each possible return a weight based on the probability that it will occur. Most investors demand a higher rate of return on investments if they perceive that there is any uncertainty about the expected rate of return. The increase in the required rate of return over the zero risk return is called as the risk . Investors want a rate of return “investor’s required or expected rate of return” that compensates them for the time, the expected rate of inflation, and the uncertainty of the return. In a more formal way this risk is the uncertainty that an investment will earn its expected rate of return. Although the required risk for investing in a asset class represents a composite of all uncertainty, it is possible to consider several fundamental sources of uncertainty including: (a) business risk, (b) liquidity risk, (c) financial risk or leverage risk, (d) exchange rate risk, and (e) country (political) risk.

Source: Bhole, L.M., and Mahakud, J. (2009), Financial institutions and markets.5th Edition, Tata McGraw Hill (India)

The objective of maximising return can be pursued only at the cost of incurring higher risk. The financial markets offer a wide range of assets from very safe to very risky, with corresponding low to high returns. The above figure shows the risk return trade-off in a capital market line example. It shows the expected return risk spectrum

5

such that the representative asset classes are arrayed over a range of risk on it. The figure shows a positive linear relationship between expected return and risk for different set of asset classes. The rational risk averse investor will chose the appropriate investment opportunity by considering the desired level of risk.

2.2. Important Concepts Related to Capital Market 1. Margin Trading: This is the part of a transaction value that a customer has equity in the transaction. Use of Margin: to buy more, to borrow money. Concepts associated with margin: Initial margin: Amount Investor Puts up / value of transaction or It is the part of transaction’s value the customer must pay to initiate the transaction with other part being borrowed from the broker. Maintenance Margin: The percentage of a security’s value that must be on hand as equity. Margin Call: Demand from the broker for additional cash or securities as a result of the actual margin declining below the maintenance margin 2. Private Placement Vs. Preferential Allotment Private placements refer to sale of equity or equity related instruments of an unlisted company or sale of debentures of a listed or unlisted company. Preferential allotments refer to sale of equity or equity related instruments of an listed company. 3. Open Outcry Trading System: Under this system traders shout and resort to signals on the trading floor of the exchange which consists of several trading posts for different securities. Buyers make their bids and sellers make their offers and bargains are closed at mutually agreed-upon prices. 4. Screen-based Trading System: Started in November 4,1994 in India. The important features are: buyers and sellers place their orders on the computer. They can be limit order or best market price order. The computer constantly tries to match mutually compatible orders on price and time priority. The limit order book or the list of unmatched limit orders is displayed on the screen. Increases efficiency, confidence and transparency in the market

5. Settling: Electronic Delivery system and it is facilitated by depositories which is an institution which dematerializes physical certificates and effects transfer of ownership by electronic book entries. Example: National Securities Depository Limited (NSDL), Central Securities Depositories Limited (CSDL) 6. Settlement Procedure: Weekly Settlement, Carry forward system (badla and undha badla), Rolling Settlement (T+1).

6

7. Badla and Undha badla: When a bull buys in the anticipation of an immediate rise in price, but finds at the end of the ing period that the price has not risen, he may either pay for the shares and take delivery, or he may carry over his transaction to the next ing period by paying carry over charges or Seedha badla to the seller. When a bear sells in anticipation of a fall in prices in the immediate future (so that he can pick up shares later for delivery and make a profit), but the fall does not happen within the ing period, he has the option to borrow or buy the shares for delivery, or have his sales carried over to the next ing period on payment of Undha badla or backwardation charges to the buyer. 8. Short Selling: In a normal transaction a security is bought and owned because the investor believes the price is likely to rise. Eventually the security is sold and the position is closed out. First you buy then you sell. A short-sell involves selling a security because of belief that the price will decline and buying back the security later to close the position. First you sell and then buy. 9. Actual selling and buying procedure: Procedure for Buying - Locating the broker----Placement of order (De-mat in a depository) then - execution of order (Contract note for tax and other legal purposes). Order may be Limit Order (upper limit of the price has been given by the investor) or Market Order (to prevail the best market price).Procedure for selling- Placement of order-- sale order----- execution of order (same as buying) 10. Important abbreviations used in stock exchange quotations: Con-Convertible, Xd- ex (excluding) dividend, Cd- cum (with) dividend, Xr- ex(excluding) right.

2.3. Importance of Stock Market Index Three major advantage: to judge the performance of individual investor, to measure the market rates of return, to predict the market movements. Factors affecting the construction of stock market index: sample, it should be representative of total population, base year, it should be a normal year, weighting criteria, equally weighted series, price weighted series, market value weighted series. Example: Stock

Quantity

Beta

Price

A

60,000

30

45

B

20,000

25

80

C

90,000

65

85

7

Solution: Equally weighted series--1/3 (45/30 + 80/ 25 + 85 / 65) = 2.0033 Price weighted series--(45 + 80 + 85)/ )(30 + 25 + 65) = 1.75 Market value weighted series = (60 000*45 + 20 000*80 + 90 000* 85) / (60 000*30 + 20 000*25 + 90 000* 65) = 1.46 Popular Stock Market Indexes in India

_____________________________________________________________________

Additional Readings:

Alexander, Gordon, J., Sharpe, William, F. and Bailey, Jeffery, V., “Fundamentals of Investment, 3rd Edition, Pearson Education. Bodie, Z., Kane, A, Marcus,A.J., and Mohanty, P. “ Investments”, 6th Edition, Tata McGraw-Hill. Bhole, L.M., and Mahakud, J. (2009), Financial institutions and markets.5th Edition, Tata McGraw Hill (India).

Fisher D.E. and Jordan R.J., “Security Analysis and Portfolio Management”, 4th Edition., Prentice-Hall. Jones, Charles, P., “Investment Analysis and Management”, 9th Edition, John Wiley and Sons. Prasanna, C., “Investment Analysis and Portfolio Management”, 3rd Edition, Tata McGraw-Hill. Reilly, Frank. and Brown, Keith, “Investment Analysis & Portfolio Management”, 7th Edition, Thomson Soth-Western.

8

__________________________________________________________ Additional Questions with Answers Session 2: Markets for Investment and Construction of Indexes ______________________________________________________________________ 1. What are the different investment alternatives provided by different financial markets? Ans. Marketable and Non-Marketable Assets: • •

Marketable: Investor can manage and control, Less Liquid in Nature: All the Market Traded Securities Non-Marketable: No management but has Right, Highly Liquid: Bank Deposits, Post office Deposits, NSC etc.

Direct Vs. Indirect Investments: • •

Direct Investment: Investor—(owns)---Portfolio--- (Dividend and Interest)--Income and Capital gain Indirect Investments: Investor—(owns)---Investment Company’s Fund--(Dividend and Interest)---Income and Capital gain

Classification of Financial Markets: • Nature of Claims: Debt Market, Equity Market • Maturity of Claims: Money Market, Capital Market • Seasoning of Claims: Primary Market, Secondary Market • Timing of Delivery: Cash or Spot Market, Forward or Futures Market • Organizational Structure: Exchange Traded Market, Over the Counter Market • 2. What is the difference between Primary market and secondary market? Ans. Primary market • The primary market is that part of the capital markets that deals with the issuance of new securities. Primary market provides opportunity to issuers of securities, Government as well as corporate, to raise resources to meet their requirements of investment and/or discharge some obligation. • Equity Capital is raised in Primary Market. It can be raised through Public or primary Issue, Right Issue, Private Placement, Preferential Allotment • The primary market is governed by the provisions of the Companies Act, 1956, which deals with issues, listing and allotment of securities. Additionally the SEBI - prescribes the eligibility and disclosure norms to be complied by the issuer, promoter for accessing the market. Secondary Market • • •

Existing securities issued in the primary market are traded This market enables participants who held securities to adjust their holdings in response to changes in their assessment of risks and returns. It operates through over-the-counter (OTC) market and the exchange traded market. 9

• •

Operation of Secondary Market: Trading , Settlement Trading: Can be Open Outcry System and/or Screen-Based System. Under Open Outcry System traders shout and resort to signals on the trading floor of the exchange which consists of several trading posts for different securities. Buyers make their bids and sellers make their offers and bargains are closed at mutually agreed-upon prices. Under Screen-Based System Buyers and sellers place their orders on the computer. They can be limit order or best market price order. The computer constantly tries to match mutually compatible orders on price and time priority. • Modern settlement system is an electronic delivery mechanism: It is facilitated by Depositories which is an institution which dematerializes physical certificates and effects transfer of ownership by electronic book entries. Settlement Procedure can be Weekly Settlement, Carry forward system (badla and undha badla), Rolling Settlement (T+1) 3. What is the meaning of margin trading and what are the major concepts associated with it? Ans. • Margin Trading: This is the part of a transaction value that a customer has equity in the transaction. Use of Margin: to buy more, to borrow money Concepts associated with margin: •

• •

Initial margin: Amount Investor Puts up / value of transaction or It is the part of transaction’s value the customer must pay to initiate the transaction with other part being borrowed from the broker. Maintenance Margin: The percentage of a security’s value that must be on hand as equity. Margin Call: Demand from the broker for additional cash or securities as a result of the actual margin declining below the maintenance margin

4. Why stock market index is importance and what are the factors affecting construction of stock market index? Ans. A good Stock Index captures the movement of the well diversified and highly liquid stocks. It is the pulse rate of the economy. Index movements reflect the changing expectations of the stock market about future dividends of the corporate sector. Importance of Stock Market Index • To judge the performance of individual investor • To measure the market rates of return • To predict the market movements Factors affecting the construction of stock market index • Sample: It should be representative of total population • Base year: It should be a normal year • Weighting criteria – Equally Weighted Series – Price Weighted Series – Market value Weighted Series

10

Related Documents 171j1w

Financial System And Financial Market 4z1j71

April 2022 0

Financial System 4o3i4y

April 2022 0

Financial Market-study Material 11dc

November 2019 86

1 Financial Market m4l5e

July 2021 0

Macroeconomics For Financial Market 5wp4i

November 2020 0

Financial Market Of Pakistan 1ky1m

October 2021 0More Documents from "Pulkit Pareek" 4u133y

Legal Profession And Ethics 6c505q

December 2019 71

Financial System And Financial Market 4z1j71

April 2022 0

Pvl101q-unit6 2t2b3z

November 2019 38

Fees Tution Onlyvit University - Vtop 6e5y2w

December 2019 49

Vb.net Tutorial 672o2x

May 2020 7