Consumer Finance 2we4c

This document was ed by and they confirmed that they have the permission to share it. If you are author or own the copyright of this book, please report to us by using this report form. Report r6l17

Overview 4q3b3c

& View Consumer Finance as PDF for free.

More details 26j3b

- Words: 3,169

- Pages: 15

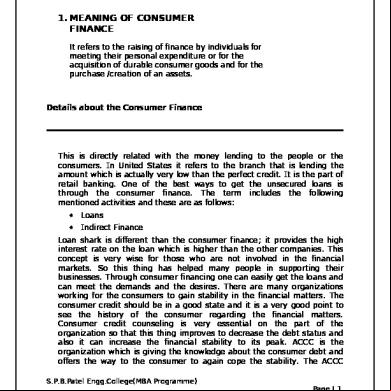

Consumer Finance 1. MEANING OF CONSUMER FINANCE It refers to the raising of finance by individuals for meeting their personal expenditure or for the acquisition of durable consumer goods and for the purchase /creation of an assets.

Details about the Consumer Finance

This is directly related with the money lending to the people or the consumers. In United States it refers to the branch that is lending the amount which is actually very low than the perfect credit. It is the part of retail banking. One of the best ways to get the unsecured loans is through the consumer finance. The term includes the following mentioned activities and these are as follows: •

Loans

•

Indirect Finance

Loan shark is different than the consumer finance; it provides the high interest rate on the loan which is higher than the other companies. This concept is very wise for those who are not involved in the financial markets. So this thing has helped many people in ing their businesses. Through consumer financing one can easily get the loans and can meet the demands and the desires. There are many organizations working for the consumers to gain stability in the financial matters. The consumer credit should be in a good state and it is a very good point to see the history of the consumer regarding the financial matters. Consumer credit counseling is very essential on the part of the organization so that this thing improves to decrease the debt status and also it can increase the financial stability to its peak. ACCC is the organization which is giving the knowledge about the consumer debt and offers the way to the consumer to again cope the stability. The ACCC S.P.B.Patel Engg.College(MBA Programme) Page | 1

Consumer Finance organization deals with large number of consumers and provides them the knowledge and information about the utilization of the credit, buying of a house etc. ACCC stands for "American consumer credit counseling". This organization has the expert and professional employees which are giving different services to the people. This organization is providing the ways to create a financial balance between the demands and the budget. It provides the information and knowledge which will enhances the financial skills and expertise of the consumer. This organization is basically a tool for a future which would free of debt so every one should get the counseling from the organization. It analyzes the financial situations of the consumers and maintains their budgets and this thing will increase the financial stability of the consumer. ACCC is one of the top organizations providing the consumer credit service in the best way. There is a lot of information consumer consolidation present in the financial internet sites. Consumer consolidation is the best way to decrease the tension, because it helps the consumer to all the loans into one and can pay back this one loan in one time, so thing makes everything simple for the consumer, and the one loan would be very easy for the consumer to repay. Consumer credit counseling service is very essential for the consumers because it gives good advices for the consumers regarding the financial matters. There are many organizations in the world which are providing consumer credit services which are helpful for the financial stability. Financial stability is very important not only for the businesses but also for the consumers. The businesses and as well as the consumers need the stability regarding the financial matters because without the stability no one could be very innovative in the longer run. Consumer credit consolidation is very helpful in making the loan repayments very easy for the consumer. Every one needs the loan now days to meet the demands of the people and the families, and obviously the stranger don't want to lend the amount to you so the Consumer credit report is enough for you to give the lender to have the loan. Consumer credit report contains all the information about the loans which you already using, and the status of the credit cards, this report also shows the unpaid bills of any card, so on the basis of the report the lender can give you the loan very easily. S.P.B.Patel Engg.College(MBA Programme) Page | 2

Consumer Finance This report is sometimes the basis for the consumer loans. If the report shows the satisfactory status then you would be easily getting the consumer loan. Consumer reporting agency is the agency that maintains the database of the credit activities of the consumer and then goes for selling it. Consumer credit agency is basically providing the information about credit activities by charging a little fee. Consumer lending is not an easy task, it is very risky in fact every thing is risky in which the money is involved. Every one can not see the credit report of yours only the following people can see on request and these are as follows: •

The lender who is going to lend money to you or have already given you.

•

Employers can see who wants to employ you.

•

Employers can see who wants it for the retention purposes.

•

The insurers can see it.

•

The agencies related with the government can see for the government benefits.

•

The third party can see it if you will sign the authority letter.

Following are the information present in the reports: •

Initial personal information

•

Information about the credit

•

Information about the public record

•

Inquiries

The banks should provide the best consumer financing information to the consumers because this thing will reduce the future hassle on the part of the consumer. The bank officers should be equipped with all the information related to the loans, taking loan is the day to day activity on the part of the borrower because the salaried person is not able to meet the demands easily; he or she has to go for loans for meeting the demands. One should keep the credit history very good for getting loans for the future purposes. Every one wants to have S.P.B.Patel Engg.College(MBA Programme) Page | 3

Consumer Finance loan for paying the bills, education purposes, business purposes etc, and one can only get the loan with the appropriate interest rate only with the good credit history.

1. IMPORTANT ASPECTS • • • • • •

consumer Parties to the transactions Modes of finance Procedure for granting of financing Purpose of raising finance Benefits of consumer finance

1.1

PARTIES TO THE TRANSACTION

• In A Bipartite Arrangement A) borrower/Consumer B) dealer Cum Financer • In A) B) C)

A Tripartite Arrangement Customer/Borrower Dealer/Sellers financer(may Be A Bank Or Non Banking Company)

Bank S.P.B.Patel Engg.College(MBA Programme) Page | 4

Consumer Finance An institution that provides a great variety of financial services. At their most basic, banks hold money on behalf of customers, which is payable to the customer on demand, either by appearing at the bank for a withdrawal or by writing a check to a third party. Banks use the money they hold to finance loans, which they make to businesses and individuals to pay for operations, mortgages, education expenses, and any number of other things. Many banks also perform other services for a fee; for instance they offer certified checks to customers guaranteeing payment to third parties. In some countries they may provide investment and insurance services. With the exception of Islamic banks, they pay interest on deposits and receive interest on their loans. Banks are regulated by the laws and central banks of their home countries; normally they must receive a charter to engage in business. Banks are usually organized as corporations.

Lender Businesses that provide loans to others. A person or organization that makes a loan. That is, a lender gives money to a borrower with the expectation of repayment in a timely manner, almost always with interest. One who advances money to another in the expectation of receiving repayment of the money plus a fee for the use of the money, called interest.

1.2

MODES OF CONSUMER FINANCE

S.P.B.Patel Engg.College(MBA Programme) Page | 5

Consumer Finance • • • •

HIRE PURCHASE INSTALMENT SYSTEM OVERDRAFT CREDIT LOANS

2.2.1 HIRE PURCHASE • Hire purchase means a transaction where goods are purchased and sold on the that 1) payment will be in installment 2) possession of goods is given immediately 3) ownership remains with sellers till the last installment paid by buyer 4) the seller can repossess the good in case of any default 5) each installment will be treaed as hire charges till the last Installment 2.2.2 RIGHTS OF HIRER • The hiree (vendor) can not terminate the hire purchase agreement The right to repossess the goods • The hirer has a right of receiving a statement • Excess payment made by the hirer will be returned by the owner to Him

S.P.B.Patel Engg.College(MBA Programme) Page | 6

Consumer Finance 2.2.3 Installment system under hire Purchase • It may be of two types 1) Conditional sale 2) Pledge or hypothecation

2.2.4 Overdraft/demand loans • Under an overdraft interest is charged on the amount actually utilized by individual customer. overdraft facility is provided against the security of life insurance policies, fixed deposits, govt. securities etc. 1) Loan against equitable mortgage of immovable property: . 2) Loan against NSC/IVP/KVP: 3) LOANS AGAINST LIFE INSURANCE POLICIES: In this loan is advanced either in form of demand loans or overdraft as 80% to 95% of the surrender value to be ascertained from insurance company. the policy has to be assigned to the bank at the time of taking credit against policy.the interest rates will vary between 11% to 12% p.a. 4)Loan against RBI relief bonds Banks and non banking finance companies also provide loans against the security of RBI relief bonds to the individual in order to meet their personal/business needs and contingencies. the loan is provided in form of term

S.P.B.Patel Engg.College(MBA Programme) Page | 7

Consumer Finance loans or overdraft. The term loan agreement may provide for the submission of: 1) 2) 3) 4)

delivery letter transfer deed endorsed bonds depository participant note

• Loan against shares and debentures: finance is provided to the individual of high credit standing against security of fully paid shares and debentures held by them, in their own name, kept in physical or dematerialized form.

2.3 Procedure for granting finance A. Pre sanction stage 1. collecting credit information 2. receiving of application form 3. analyzing customer’s credit worthiness 4. accepting/rejecting applications 5. entering into a contract B. Post sanction stage a) submission of documents b) payment of credit/finance c) payment of installments

2.4 of financing These include the following: 1. Amount of loan/credit S.P.B.Patel Engg.College(MBA Programme) Page | 8

Consumer Finance 2. 3. 4. 5. 6. 7. 8.

Margin requirements Security Period of finance Rate of interest Fees and charges Mode of payment documentation

2.5 Purpose of Raising Finance Housing Finance It refers to providing finance to the individual or group of individuals for the purchase, construction or related activities of house/flat etc. The housing loan is a type of instalment credit which forms the largest single source of housing finance. • The housing loan can be availed for following purposes:• Construction • Extension • Purchase • Combined loan for purchase of plot and construction • Acquired house through cooperative housing society Rate of Interest • Fixed rate of interest loan • Floating or variable rate of interest loan Charges & Fees payable • Processing fees • Search report charges by the advocate at the time of sanction • Insurance charges • Fine for non-payment of late payment of instalments Security for the loan • Primary security S.P.B.Patel Engg.College(MBA Programme) Page | 9

Consumer Finance • Collateral security • Interim security Institutions providing housing finance • IDBI • HDFC • ICICI • SBI • LIC Housing Finance • Tata Home Finance

Parameters of the best house loan • • • • • • • •

Lower interest rate Income tax incentive Longest tenure Lowest margin Complete doorstep service no pre-payment charges Discount on processing fee Concession in credit card/ ATM card fees

Educational Loans The prime aim is to make careers happen. The no. of students seeking ission to professional courses is multiplying every year. If one has the ambition and drive, the banks will take care of finances involved. Eligibility Criteria • Should be an Indian national • Belongs to the age group of 16-40 years S.P.B.Patel Engg.College(MBA Programme) Page | 10

Consumer Finance • Has secured ission in a Professional/technical course, • foreign university/institution • Should have secured minimum 60% marks in the previous qualifying examination Objectives of finance • • • •

To To To To

finance all fees meet expenses provide financial assistance cover course fee, hostel and mess charges

Processing fees SBI, CBI, BOB – do not charge any fees HSBC and Bank of Punjab – 1% of the loan Repayment Period 5 -7 years after commencement of Repayment Automobile Finance Under the banks auto loan scheme there is a vehicle loan for every class i.e. 2 wheeler’s loan, 2nd hand car loans, new car loan. The market for auto loans is large and lot of opportunity exists there for the banks and other finance companies who by adopting customer friendly policies and mass advertising can surely make auto loan scheme a success. Eligibility

S.P.B.Patel Engg.College(MBA Programme) Page | 11

Consumer Finance • Permanent employees of govt., Public/private sector with minimum of 3years service. • Professionals and self employed such as doctors, CASs, MBAs etc. • Persons engaged in agricultural and allied activities. Purpose Auto loans are extended for the purchase of vehicle both for personal and professional use. Type of loan Finance is provided in form of term loans extending for a period from 1 to 5 years. Rate of interest Varies from bank to bank Insurance A insurance policy is taken for market value or 10% above the loan amount whichever is higher .

Processing Charges Most of the banks do not charge any processing fee, or Rs. 250 to Rs. 500 may be collected as one time fee from the customers. Personal Loans General purpose loans are advanced to the individual to meet personal expenses. Thus, with such easy finance facility, a consumer can buy whatever he has in mind. S.P.B.Patel Engg.College(MBA Programme) Page | 12

Consumer Finance Eligibility Criteria • Salaried employees • Self employed professionals such as Doctors, CAs, MBAs, etc. Loan amount Minimum – Rs.25000 Maximum – Rs. 10,00,000 Other features • No security or guarantor required • Repayment period 12 to 48 months • Speedy approval Finance to meet Festival Expenses The lower or middle income group of individuals who cannot satisfy the requirements of the personal loan scheme seek financial assistance from the banks for short duration to meet expenditure relating to a festival. The bank may charge nominal fee of Rs.100 per application. Eligibility Criteria • Employees of govt. / Profit making Public / institutions. Etc. with a minimum of 2 years service. • Self employed persons • Persons having regular source of income from verifiable sources like pension and interest from govt. securities etc. Holiday Finance Today, consumer who finds himself unable to meet the cost of package gets ready to accept the option. For ex, SOTC’s European tour package is priced at over Rs.76,000. S.P.B.Patel Engg.College(MBA Programme) Page | 13

Consumer Finance Finance for Medical Treatment It is very difficult for individuals especially the salaried class to arrange funds at short notice to make payments to hospitals. Banks extend loans to meet such exigencies. Loans are available to all such patients who are suffering from diseases where mortality probability is low and the patient emerges as a healthier person after treatment.

2.6 Benefits of Consumer Finance • • • •

Rising standard of living Forced savings Help consumes meet emergencies Increase in demand for physical goods

Profit Revenue minus cost. The amount one makes on a transaction. A company's total revenue less its operating expenses, interest paid, depreciation, and taxes. For example, suppose a widget manufacturer earns $1,000,000 in total revenue. The widgets cost $200,000 to make and his istrative and payroll expenses total $250,000. He also must subtract $50,000 in depreciation on his widget manufacturing equipment and pay $200,000 in taxes. His net income is stated as: $1,000,000 $200,000 - $250,000 - $50,000 - $200,000 = $300,000. Profit, which is also called net income or earnings, is the money a business has left after it pays its operating expenses, taxes, and other current bills. When you invest, profit is the amount you make when you sell an asset for a higher price than you paid for it. For example, if you buy a stock at

S.P.B.Patel Engg.College(MBA Programme) Page | 14

Consumer Finance $20 a share and sell it at $30 a share, your profit is $10 a share minus sales commission and capital gains tax if any. Interest The price paid for borrowing money. It is expressed as a percentage rate over a period of time and reflects the rate of exchange of present consumption for future consumption. Also, a share or title in property. 1. Payment for the use of borrowed money. 2. An investor's equity in a business. Money that is paid in exchange for borrowing or using another person?s or organization's money. Interest is calculated as a percentage of the money borrowed. There are two kinds of interest, simple interest and compound interest. In simple interest, the interest is calculated only over the original principal amount. For example, if one borrows $1000 at 3% interest, the interest is $30 (3% of $1000) each time it is calculated. In compound interest, interest previously paid is included in the calculation of future interest. For example, with the above loan, interest paid in the first month is $30 (3% of $1000), in the second month it is $30.90 (3% of $1030), and so forth. Compound interest is more common because it yields more for the lender. Interest is what you pay to borrow money using a loan, credit card, or line of credit. It is calculated at either a fixed or variable rate that's expressed as a percentage of the amount you borrow, pegged to a specific time period. For example, you may pay 1.2% interest monthly on the unpaid balance of your credit card. Interest also refers to the income, figured as a percentage of principal, that you're paid for purchasing a bond, keeping money in a bank , or making other interest-paying investments. If it is simple interest, earnings are figured on the principal. If it is compound interest, the earnings are added to the principal to form a new base on which future income is calculated. Interest is also a share or right in a property or asset. For example, if you are half-owner of a vacation home, you have a 50% interest. Sums paid or earned for the use of money.

S.P.B.Patel Engg.College(MBA Programme) Page | 15

Details about the Consumer Finance

This is directly related with the money lending to the people or the consumers. In United States it refers to the branch that is lending the amount which is actually very low than the perfect credit. It is the part of retail banking. One of the best ways to get the unsecured loans is through the consumer finance. The term includes the following mentioned activities and these are as follows: •

Loans

•

Indirect Finance

Loan shark is different than the consumer finance; it provides the high interest rate on the loan which is higher than the other companies. This concept is very wise for those who are not involved in the financial markets. So this thing has helped many people in ing their businesses. Through consumer financing one can easily get the loans and can meet the demands and the desires. There are many organizations working for the consumers to gain stability in the financial matters. The consumer credit should be in a good state and it is a very good point to see the history of the consumer regarding the financial matters. Consumer credit counseling is very essential on the part of the organization so that this thing improves to decrease the debt status and also it can increase the financial stability to its peak. ACCC is the organization which is giving the knowledge about the consumer debt and offers the way to the consumer to again cope the stability. The ACCC S.P.B.Patel Engg.College(MBA Programme) Page | 1

Consumer Finance organization deals with large number of consumers and provides them the knowledge and information about the utilization of the credit, buying of a house etc. ACCC stands for "American consumer credit counseling". This organization has the expert and professional employees which are giving different services to the people. This organization is providing the ways to create a financial balance between the demands and the budget. It provides the information and knowledge which will enhances the financial skills and expertise of the consumer. This organization is basically a tool for a future which would free of debt so every one should get the counseling from the organization. It analyzes the financial situations of the consumers and maintains their budgets and this thing will increase the financial stability of the consumer. ACCC is one of the top organizations providing the consumer credit service in the best way. There is a lot of information consumer consolidation present in the financial internet sites. Consumer consolidation is the best way to decrease the tension, because it helps the consumer to all the loans into one and can pay back this one loan in one time, so thing makes everything simple for the consumer, and the one loan would be very easy for the consumer to repay. Consumer credit counseling service is very essential for the consumers because it gives good advices for the consumers regarding the financial matters. There are many organizations in the world which are providing consumer credit services which are helpful for the financial stability. Financial stability is very important not only for the businesses but also for the consumers. The businesses and as well as the consumers need the stability regarding the financial matters because without the stability no one could be very innovative in the longer run. Consumer credit consolidation is very helpful in making the loan repayments very easy for the consumer. Every one needs the loan now days to meet the demands of the people and the families, and obviously the stranger don't want to lend the amount to you so the Consumer credit report is enough for you to give the lender to have the loan. Consumer credit report contains all the information about the loans which you already using, and the status of the credit cards, this report also shows the unpaid bills of any card, so on the basis of the report the lender can give you the loan very easily. S.P.B.Patel Engg.College(MBA Programme) Page | 2

Consumer Finance This report is sometimes the basis for the consumer loans. If the report shows the satisfactory status then you would be easily getting the consumer loan. Consumer reporting agency is the agency that maintains the database of the credit activities of the consumer and then goes for selling it. Consumer credit agency is basically providing the information about credit activities by charging a little fee. Consumer lending is not an easy task, it is very risky in fact every thing is risky in which the money is involved. Every one can not see the credit report of yours only the following people can see on request and these are as follows: •

The lender who is going to lend money to you or have already given you.

•

Employers can see who wants to employ you.

•

Employers can see who wants it for the retention purposes.

•

The insurers can see it.

•

The agencies related with the government can see for the government benefits.

•

The third party can see it if you will sign the authority letter.

Following are the information present in the reports: •

Initial personal information

•

Information about the credit

•

Information about the public record

•

Inquiries

The banks should provide the best consumer financing information to the consumers because this thing will reduce the future hassle on the part of the consumer. The bank officers should be equipped with all the information related to the loans, taking loan is the day to day activity on the part of the borrower because the salaried person is not able to meet the demands easily; he or she has to go for loans for meeting the demands. One should keep the credit history very good for getting loans for the future purposes. Every one wants to have S.P.B.Patel Engg.College(MBA Programme) Page | 3

Consumer Finance loan for paying the bills, education purposes, business purposes etc, and one can only get the loan with the appropriate interest rate only with the good credit history.

1. IMPORTANT ASPECTS • • • • • •

consumer Parties to the transactions Modes of finance Procedure for granting of financing Purpose of raising finance Benefits of consumer finance

1.1

PARTIES TO THE TRANSACTION

• In A Bipartite Arrangement A) borrower/Consumer B) dealer Cum Financer • In A) B) C)

A Tripartite Arrangement Customer/Borrower Dealer/Sellers financer(may Be A Bank Or Non Banking Company)

Bank S.P.B.Patel Engg.College(MBA Programme) Page | 4

Consumer Finance An institution that provides a great variety of financial services. At their most basic, banks hold money on behalf of customers, which is payable to the customer on demand, either by appearing at the bank for a withdrawal or by writing a check to a third party. Banks use the money they hold to finance loans, which they make to businesses and individuals to pay for operations, mortgages, education expenses, and any number of other things. Many banks also perform other services for a fee; for instance they offer certified checks to customers guaranteeing payment to third parties. In some countries they may provide investment and insurance services. With the exception of Islamic banks, they pay interest on deposits and receive interest on their loans. Banks are regulated by the laws and central banks of their home countries; normally they must receive a charter to engage in business. Banks are usually organized as corporations.

Lender Businesses that provide loans to others. A person or organization that makes a loan. That is, a lender gives money to a borrower with the expectation of repayment in a timely manner, almost always with interest. One who advances money to another in the expectation of receiving repayment of the money plus a fee for the use of the money, called interest.

1.2

MODES OF CONSUMER FINANCE

S.P.B.Patel Engg.College(MBA Programme) Page | 5

Consumer Finance • • • •

HIRE PURCHASE INSTALMENT SYSTEM OVERDRAFT CREDIT LOANS

2.2.1 HIRE PURCHASE • Hire purchase means a transaction where goods are purchased and sold on the that 1) payment will be in installment 2) possession of goods is given immediately 3) ownership remains with sellers till the last installment paid by buyer 4) the seller can repossess the good in case of any default 5) each installment will be treaed as hire charges till the last Installment 2.2.2 RIGHTS OF HIRER • The hiree (vendor) can not terminate the hire purchase agreement The right to repossess the goods • The hirer has a right of receiving a statement • Excess payment made by the hirer will be returned by the owner to Him

S.P.B.Patel Engg.College(MBA Programme) Page | 6

Consumer Finance 2.2.3 Installment system under hire Purchase • It may be of two types 1) Conditional sale 2) Pledge or hypothecation

2.2.4 Overdraft/demand loans • Under an overdraft interest is charged on the amount actually utilized by individual customer. overdraft facility is provided against the security of life insurance policies, fixed deposits, govt. securities etc. 1) Loan against equitable mortgage of immovable property: . 2) Loan against NSC/IVP/KVP: 3) LOANS AGAINST LIFE INSURANCE POLICIES: In this loan is advanced either in form of demand loans or overdraft as 80% to 95% of the surrender value to be ascertained from insurance company. the policy has to be assigned to the bank at the time of taking credit against policy.the interest rates will vary between 11% to 12% p.a. 4)Loan against RBI relief bonds Banks and non banking finance companies also provide loans against the security of RBI relief bonds to the individual in order to meet their personal/business needs and contingencies. the loan is provided in form of term

S.P.B.Patel Engg.College(MBA Programme) Page | 7

Consumer Finance loans or overdraft. The term loan agreement may provide for the submission of: 1) 2) 3) 4)

delivery letter transfer deed endorsed bonds depository participant note

• Loan against shares and debentures: finance is provided to the individual of high credit standing against security of fully paid shares and debentures held by them, in their own name, kept in physical or dematerialized form.

2.3 Procedure for granting finance A. Pre sanction stage 1. collecting credit information 2. receiving of application form 3. analyzing customer’s credit worthiness 4. accepting/rejecting applications 5. entering into a contract B. Post sanction stage a) submission of documents b) payment of credit/finance c) payment of installments

2.4 of financing These include the following: 1. Amount of loan/credit S.P.B.Patel Engg.College(MBA Programme) Page | 8

Consumer Finance 2. 3. 4. 5. 6. 7. 8.

Margin requirements Security Period of finance Rate of interest Fees and charges Mode of payment documentation

2.5 Purpose of Raising Finance Housing Finance It refers to providing finance to the individual or group of individuals for the purchase, construction or related activities of house/flat etc. The housing loan is a type of instalment credit which forms the largest single source of housing finance. • The housing loan can be availed for following purposes:• Construction • Extension • Purchase • Combined loan for purchase of plot and construction • Acquired house through cooperative housing society Rate of Interest • Fixed rate of interest loan • Floating or variable rate of interest loan Charges & Fees payable • Processing fees • Search report charges by the advocate at the time of sanction • Insurance charges • Fine for non-payment of late payment of instalments Security for the loan • Primary security S.P.B.Patel Engg.College(MBA Programme) Page | 9

Consumer Finance • Collateral security • Interim security Institutions providing housing finance • IDBI • HDFC • ICICI • SBI • LIC Housing Finance • Tata Home Finance

Parameters of the best house loan • • • • • • • •

Lower interest rate Income tax incentive Longest tenure Lowest margin Complete doorstep service no pre-payment charges Discount on processing fee Concession in credit card/ ATM card fees

Educational Loans The prime aim is to make careers happen. The no. of students seeking ission to professional courses is multiplying every year. If one has the ambition and drive, the banks will take care of finances involved. Eligibility Criteria • Should be an Indian national • Belongs to the age group of 16-40 years S.P.B.Patel Engg.College(MBA Programme) Page | 10

Consumer Finance • Has secured ission in a Professional/technical course, • foreign university/institution • Should have secured minimum 60% marks in the previous qualifying examination Objectives of finance • • • •

To To To To

finance all fees meet expenses provide financial assistance cover course fee, hostel and mess charges

Processing fees SBI, CBI, BOB – do not charge any fees HSBC and Bank of Punjab – 1% of the loan Repayment Period 5 -7 years after commencement of Repayment Automobile Finance Under the banks auto loan scheme there is a vehicle loan for every class i.e. 2 wheeler’s loan, 2nd hand car loans, new car loan. The market for auto loans is large and lot of opportunity exists there for the banks and other finance companies who by adopting customer friendly policies and mass advertising can surely make auto loan scheme a success. Eligibility

S.P.B.Patel Engg.College(MBA Programme) Page | 11

Consumer Finance • Permanent employees of govt., Public/private sector with minimum of 3years service. • Professionals and self employed such as doctors, CASs, MBAs etc. • Persons engaged in agricultural and allied activities. Purpose Auto loans are extended for the purchase of vehicle both for personal and professional use. Type of loan Finance is provided in form of term loans extending for a period from 1 to 5 years. Rate of interest Varies from bank to bank Insurance A insurance policy is taken for market value or 10% above the loan amount whichever is higher .

Processing Charges Most of the banks do not charge any processing fee, or Rs. 250 to Rs. 500 may be collected as one time fee from the customers. Personal Loans General purpose loans are advanced to the individual to meet personal expenses. Thus, with such easy finance facility, a consumer can buy whatever he has in mind. S.P.B.Patel Engg.College(MBA Programme) Page | 12

Consumer Finance Eligibility Criteria • Salaried employees • Self employed professionals such as Doctors, CAs, MBAs, etc. Loan amount Minimum – Rs.25000 Maximum – Rs. 10,00,000 Other features • No security or guarantor required • Repayment period 12 to 48 months • Speedy approval Finance to meet Festival Expenses The lower or middle income group of individuals who cannot satisfy the requirements of the personal loan scheme seek financial assistance from the banks for short duration to meet expenditure relating to a festival. The bank may charge nominal fee of Rs.100 per application. Eligibility Criteria • Employees of govt. / Profit making Public / institutions. Etc. with a minimum of 2 years service. • Self employed persons • Persons having regular source of income from verifiable sources like pension and interest from govt. securities etc. Holiday Finance Today, consumer who finds himself unable to meet the cost of package gets ready to accept the option. For ex, SOTC’s European tour package is priced at over Rs.76,000. S.P.B.Patel Engg.College(MBA Programme) Page | 13

Consumer Finance Finance for Medical Treatment It is very difficult for individuals especially the salaried class to arrange funds at short notice to make payments to hospitals. Banks extend loans to meet such exigencies. Loans are available to all such patients who are suffering from diseases where mortality probability is low and the patient emerges as a healthier person after treatment.

2.6 Benefits of Consumer Finance • • • •

Rising standard of living Forced savings Help consumes meet emergencies Increase in demand for physical goods

Profit Revenue minus cost. The amount one makes on a transaction. A company's total revenue less its operating expenses, interest paid, depreciation, and taxes. For example, suppose a widget manufacturer earns $1,000,000 in total revenue. The widgets cost $200,000 to make and his istrative and payroll expenses total $250,000. He also must subtract $50,000 in depreciation on his widget manufacturing equipment and pay $200,000 in taxes. His net income is stated as: $1,000,000 $200,000 - $250,000 - $50,000 - $200,000 = $300,000. Profit, which is also called net income or earnings, is the money a business has left after it pays its operating expenses, taxes, and other current bills. When you invest, profit is the amount you make when you sell an asset for a higher price than you paid for it. For example, if you buy a stock at

S.P.B.Patel Engg.College(MBA Programme) Page | 14

Consumer Finance $20 a share and sell it at $30 a share, your profit is $10 a share minus sales commission and capital gains tax if any. Interest The price paid for borrowing money. It is expressed as a percentage rate over a period of time and reflects the rate of exchange of present consumption for future consumption. Also, a share or title in property. 1. Payment for the use of borrowed money. 2. An investor's equity in a business. Money that is paid in exchange for borrowing or using another person?s or organization's money. Interest is calculated as a percentage of the money borrowed. There are two kinds of interest, simple interest and compound interest. In simple interest, the interest is calculated only over the original principal amount. For example, if one borrows $1000 at 3% interest, the interest is $30 (3% of $1000) each time it is calculated. In compound interest, interest previously paid is included in the calculation of future interest. For example, with the above loan, interest paid in the first month is $30 (3% of $1000), in the second month it is $30.90 (3% of $1030), and so forth. Compound interest is more common because it yields more for the lender. Interest is what you pay to borrow money using a loan, credit card, or line of credit. It is calculated at either a fixed or variable rate that's expressed as a percentage of the amount you borrow, pegged to a specific time period. For example, you may pay 1.2% interest monthly on the unpaid balance of your credit card. Interest also refers to the income, figured as a percentage of principal, that you're paid for purchasing a bond, keeping money in a bank , or making other interest-paying investments. If it is simple interest, earnings are figured on the principal. If it is compound interest, the earnings are added to the principal to form a new base on which future income is calculated. Interest is also a share or right in a property or asset. For example, if you are half-owner of a vacation home, you have a 50% interest. Sums paid or earned for the use of money.

S.P.B.Patel Engg.College(MBA Programme) Page | 15

Related Documents 171j1w

Consumer Finance 2we4c

November 2019 16

Business Model - Consumer Finance 3k2b1q

February 2022 0

Presentation On Consumer Finance 5n5b3u

November 2019 27

Consumer Finance At Bank Alfalah.ppt 2k494m

March 2021 0

Hire Purchase Finance And Consumer Credit 1h16p

December 2019 17